Detroit automakers are severely overstocked and ready to go on strike.

Written by Wolf Richter of Wolf Street.

According to Cox Automotive, the average transaction price (ATP) of Tesla models in the US in August fell 19.5% from the same month last year. Most EV manufacturers have been aiming for higher price points. Because they thought it would be easy to make money. However, luxury goods are gradually declining due to Tesla’s price attack.

ATP for all EVs has fallen nearly 18% year over year, falling from over $65,000 in August last year to $53,376 in August of this year. These are significant price declines that are starting to impact the overall market.

Other automakers have also implemented effective price reductions through increased incentive spending, with ATP across all brands at $48,451, roughly unchanged year-over-year, according to Cox Automotive.

For the first eight months of 2023, ATP across all brands decreased by 2.4% or $1,212, the largest data decline since 2012.

The table below shows ATP by car manufacturer. Four of them show a year-over-year decrease in ATP. Chinese automaker Geely owns Volvo and controls Polestar. Indian car manufacturer Tata owns Jaguar Land Rover. Volkswagen Group of America includes Volkswagen, Audi, Bentley, Bugatti, and Lamborghini.

| ATP year-on-year change (%) | |

| tesla | -19.5% |

| Nissan/Mitsubishi | -4.9% |

| geely | -4.0% |

| Honda | -2.9% |

| mazda | 0.1% |

| Toyota | 0.1% |

| GM | 0.6% |

| Subaru | 1.5% |

| hyundai | 2.9% |

| ford | 4.4% |

| Stellantis | 4.7% |

| bmw group | 6.2% |

| Tata | 7.8% |

| Mercedes-Benz | 12.4% |

| volkswagen group | 13.9% |

Consumers are hungry for lower prices, causing a surge in sales.

Tesla only discloses its global deliveries, which saw an 83% year-over-year increase in the second quarter. Estimates are that Tesla’s year-over-year growth in the U.S. alone is expected to be around 40%. California saw a 37% year-over-year increase in new Tesla registrations in the second quarter, according to the CNCDA.

The proportion of EVs in the total number of registered vehicles in California has reached 21%. Tesla’s Model Y and Model 3 were the number one bestseller and his number two last year, but they have widened their lead this year.

Thanks to the price cuts, Tesla has a 13.6% market share in California, making it the second-largest automaker behind Toyota’s 14.7% market share. The third largest car manufacturer is Honda, with a market share of 9.3%. At this pace, Tesla will be number one in 2024.

As it turns out, lower prices are just what the doctor ordered, a bitter pill for traditional automakers with oligopolistic pricing methods. Consumers prefer low prices.

U.S. vehicle deliveries across all brands rose 17% in August from a year earlier, according to data from the U.S. Bureau of Economic Analysis.

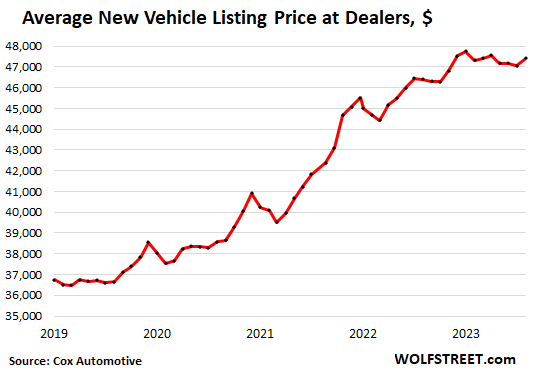

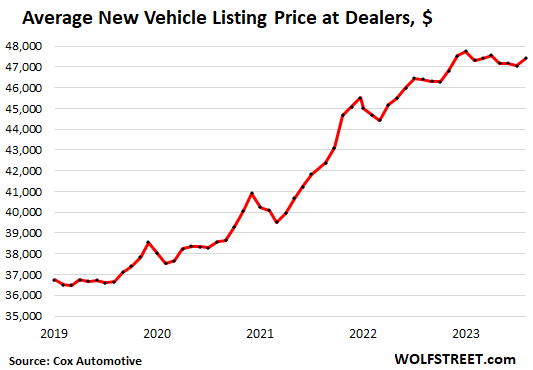

Another measure: average listing price August is just a few days away from 2023.

However, the average listing price soared 30% in the three years from the end of 2019 to 2022, after already rising sharply the previous year. These large price increases are truly harmful.

So, after years of harmful price increases, let’s move on.

Very little left below $20,000. The least expensive cars in the United States are the Mitsubishi Mirage and Kia Rio, both of which start in the $17,000 range. Most other automakers have abandoned this segment.

Below $30,000 is thin. Only three segments had ATPs below $30,000 in August: compact cars, subcompact cars, and subcompact SUVs. Bolt and Bolt EUV belong to this category.

Prices for lower-end models in other segments, such as Ford’s Maverick pickup truck, start in the sub-$30,000 range. However, when looking at the ATP for the entire segment, only compact cars, subcompact cars, and subcompact SUVs are under $30,000.

ATP for non-luxury cars Cox said sales rose 0.7% from the previous year to $44,827.

Three best-selling segments Although it accounted for 45% of total sales in August, ATP was much higher.

- Compact SUV: $35,688

- Midsize SUV: $46,381

- Full-size pickup: $65,567.

Luxury car ATP It was $64,107, down 3.3% from the same period last year. Tesla’s price cuts were dominant. Other brands in this segment that saw declines in ATP include Buick, Infiniti, Jaguar, and Volvo. However, Audi and Mercedes-Benz’s ATP increased by 10% year-over-year, BMW’s increased by 6%, and Cadillac, Land Rover, Lexus, and Lincoln’s ATP also increased.

Tesla is building factories and expanding production at existing factories, driving sales with brutally low prices in an industry that loves to raise prices.

Tesla had the highest profit margin of any major automaker before the price cut, so it can afford to lower prices. And the company’s price cuts, followed by many other EV makers, are starting to have a cleansing effect on all automakers whose oligopolistic pricing practices have led to years of harmful price increases.

These automakers have been poised for change by new entrants, and now they’re being shaken up, and that’s a good thing. New car prices need to return to normal. And we’re going to keep watching to see how that goes.

Reigniting the sub-$30,000 segment.

What the market needs now is a flood of non-luxury EV models that will put price pressure on the lower end of the ICE range. Even the Model 3 is in the “semi-luxury” segment and competes directly with the BMW 3 Series, not the Toyota Corolla.

GM’s Bolt costs well under $30,000, but its model run ends by the end of this year. GM teased a new Bolt based on GM’s new Ultium platform, also in the sub-$30,000 range. Tesla is rumored to release a model manufactured in Mexico that costs less than $30,000. And other automakers are sure to join the fray. So eventually, if not now, there will be some serious effort in this sub-$30,000 price category that ICE vehicles have been abandoning one by one.

And maybe some Chinese EV makers can find a way to create a fight for the sub-$20,000 segment in the US?

Incentive spending by automakers is increasing.

Domestic automakers, who currently have excess inventory on many models (more on that later), are piling up incentives, a way to lower prices during a model year without changing the manufacturer’s suggested retail price. Incentive spending jumped to an average of $2,365 per vehicle in August, representing about 4.9% of average transaction price (ATP). However, there is still a long way to go before incentive spending reaches the 10% of ATP needed in 2019 to move inventory.

However, the incentives for some models are much higher, reaching more than 10% of ATP in the luxury car segment, 8% for luxury cars, 7.3% for entry-level cars, and 6.1% for full-size pickup trucks.

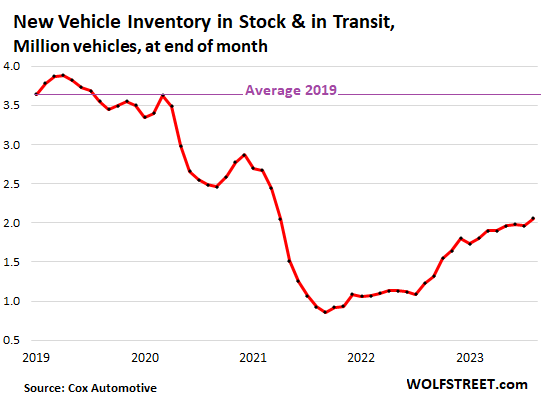

Inventories recovered and Detroit brands were overstocked and ready for a strike.

Inventory at dealers and in transit increased to 2.06 million units, the highest level since March 2021. Supply has increased to a maximum of 58 days, with 60 days of supply considered healthy. However, it is very skewed, with some brands having low inventory and others having excess inventory.

Inventories were extremely high in 2019, exceeding 3.5 million units for most of the year, with supplies ranging from 80 to 95 days.

However, EV inventories of pure EV manufacturers are not included. There is a lot of confusion regarding EV inventory. Pure EV manufacturers (Tesla, Rivian, Polestar, etc.) do not have dealers. They sell directly to consumers and do not publish their inventory. Cox Automotive does not keep track of its own inventory data and does not include it in its metrics.

So if you read anything about EV inventory or EV supply, it’s about legacy automakers like Ford EVs, GM EVs, Kia EVs, which are still completely dominated by Tesla. This is just one corner of the EV market. .

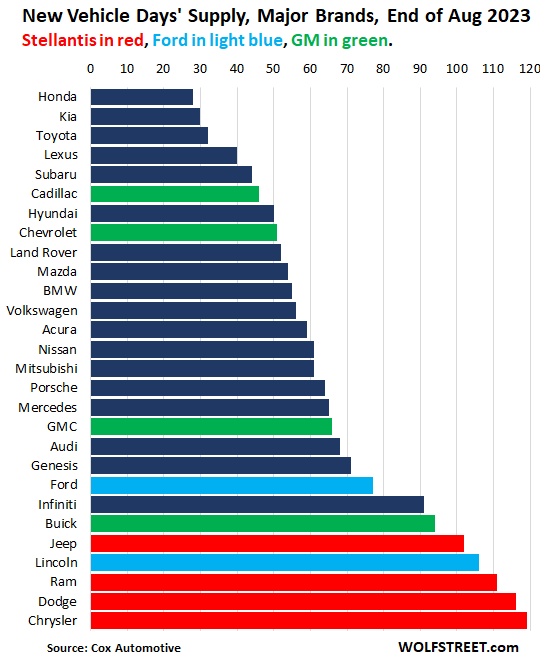

The Chevrolet Volt, one of the legacy automaker’s best-selling non-Tesla EVs, has less than 30 days of supply, meaning many dealers are essentially out of stock.

We have a wide range of inventory by brand. Honda, Kia, and Toyota dealers were almost out of stock, but the Stellantis (red) brand was severely overstocked.

The Stellantis brand, which is stuck in inventory, may be able to weather the UAW strike for some time before inventory clearing eventually impacts sales. The situation is more complicated at GM and Ford, where a strike could hit sales of some models fairly quickly.

Tesla and other EV brands that don’t have dealers are not included here.

Enjoy reading and supporting Wolf Street? You can donate. I appreciate it very much. Click on the beer and iced tea mugs to see how.

Would you like to receive email notifications when new articles are published on WOLFSTREET? Sign up here.

![]()