Those who can, pay in cash to avoid interest charges. Subprime credit will be tightened significantly.

Written by Wolf Richter of Wolf Street.

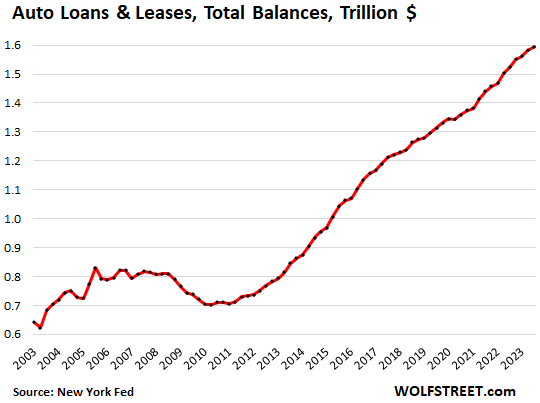

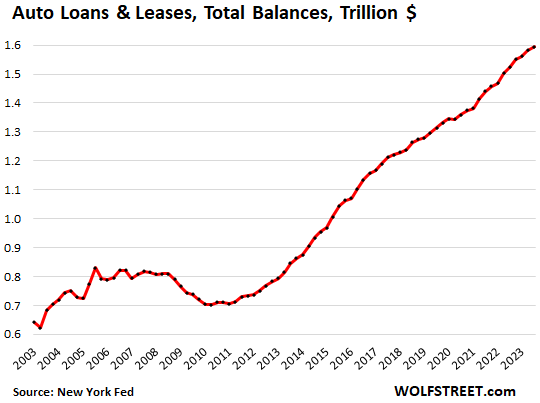

Auto loan and lease balances totaled 1.6 trillion in the third quarter, up 0.8% from the second quarter and up 4.7% from a year earlier, according to New York Fed Household Debt and Credit Report data. Ta. This is said to be due to financing for new cars. .

New cars account for the majority of car loans and car leases. New car prices continued to rise in the third quarter, with new car sales increasing 20% year over year. That’s where the increase in loans and leases comes from.

In contrast, used car prices have been declining since their outrageous rise through 2021, and used car retail sales in the third quarter were almost flat compared to the same period last year. Used cars do not contribute to the increase in auto loan balances.

More and more buyers are paying with cash. Borrowing is less attractive because interest rates are much higher. For new cars, automakers’ captive finance units are cutting interest rates to as low as 1.9%. However, this is an incentive that replaces cash incentives such as the large rebates available to cash buyers. As a result, the proportion of cash buyers for both new and used cars has increased this year.

About 20% of new car buyers and 61% of used car buyers paid for their car purchases with cash, up from 16.5% and 58.5%, respectively, in the same period last year, according to Experian’s second quarter report on auto financing. And these buyers have no debt burden associated with their cars.

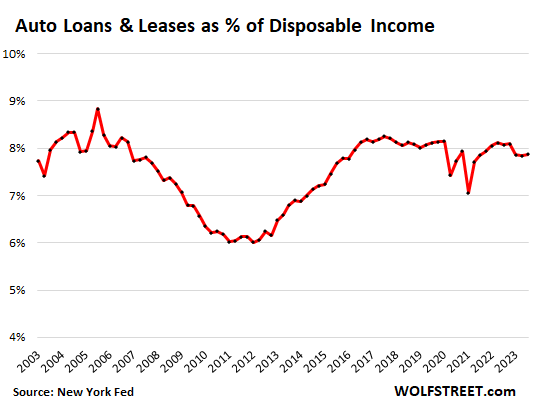

Debt burden decreased this year. In terms of total debt, auto loan and lease balances amounted to 7.9% of total disposable income, slightly lower than during the pre-pandemic boom years.

Disposable income is income from all sources, excluding capital gains, less taxes and social insurance contributions. This is the cash that consumers have left over to spend on things like cars.

This year’s fairly sharp decline in debt burden ratios is due to the largest pay increase in 40 years, as well as an increase in the proportion of cash buyers.

Confidence in subprime has tightened significantly.. Among auto loans, subprime loans are facing tougher financial conditions. Financing has become harder to obtain, some of the most aggressive lenders/dealers have filed for bankruptcy, and others have stepped up subprime underwriting. Losses lead to more prudent underwriting, which ultimately leads to lower losses. This is part of the subprime cycle.

As a result, the proportion of subprime loans in total loans has declined. According to Experian’s second quarter report, subprime as a percentage of total loan and lease originations fell to 15.0%, down from 16.8% a year ago and 17.8% two years ago.

Prime borrowers are fine. I loaned and leased cars, but cheap money is gone.

Borrowers pay through the nose: The average interest rate on a 72-month new car loan jumped from 4.84% in February 2022, before the rate hikes began, to 8.12% in August 2023, according to commercial bank data collected by the Federal Reserve.

But it’s not as shocking as it sounds. For example, if you financed $40,000 at 4.84% for 72 months, your payments would be $642 per month. At 8.12%, your payment is $704. We can already hear you saying, “For just $62 more per month, your dreams can become a reality.” And people want their dreams.

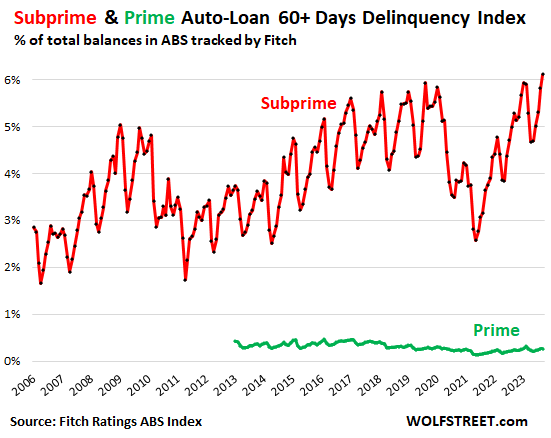

Delinquencies are caused by subprime. Subprimes always face more or less difficulty. That’s why it’s subprime. In the auto loan market, selling and financing to customers with subprime credit ratings is a high-risk, high-return specialized activity that is primarily limited to older, used vehicles. This has attracted a cluster of specialist lenders and dealers, often backed by PE firms. The system relies on the ability to securitize subprime auto loans into asset-backed securities (ABS) and sell investment-grade tranches of ABS at relatively low yields to pension funds and other yield-seeking institutional investors. and it works until it works. ‘t, and now it’s not.

Many of those ABS deals were recently scrapped, and some were only renegotiated and then withdrawn. Also, some of those specialty businesses have filed for bankruptcy, and we’ve highlighted some of them here.

There has been a unique subprime cycle, where low yields have made specialty companies very aggressive and encouraged them to take huge risks, supported by yield-hungry investors buying ABS. But after a while, those trades were so aggressive that risks come home to roost, investors take losses, become cautious, and the whole math starts to sort of unravel. It happened in 2018 and it will happen again.

But subprime is only a small part of the car financing business, and an even smaller part of the car sales business because many people pay in cash. Of the buyers with financing, new For cars, only about 5% is subprime.and those who provide financing Already used According to Experian, 22% of cars are subprime.

And the number of subprime loans that are at least 60 days past due sharply increased through September (red line). But ABS-backed auto loans tracked by Fitch Ratings show that prime loans are rock solid with modest and stable delinquency rates below pre-pandemic levels.

Overall delinquency rate Auto loans and leases are always much more expensive than home loans, but they are still lower than credit card delinquency rates.

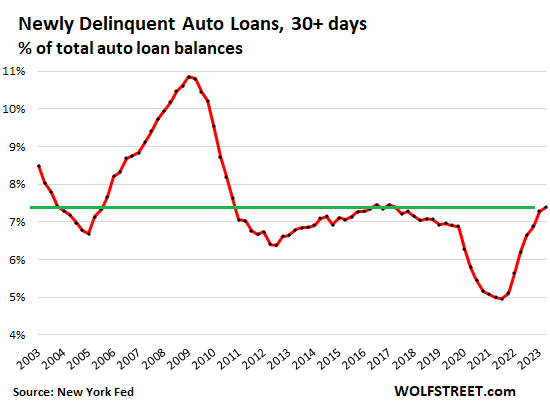

Auto loans and leases that just went into delinquency by the end of the third quarter increased by 11 basis points from 7.28% in the previous quarter, the slowest growth since they started increasing in the first quarter of 2022. So they are almost back to normal range.

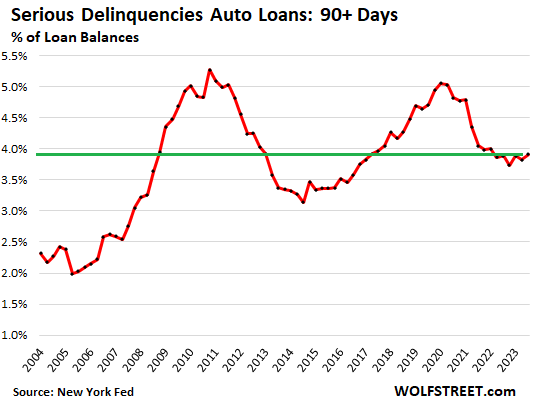

Serious auto loans that were 90 days or more past due by the end of the third quarter increased little in the third quarter after declining in the second quarter and are relatively low compared to the past 15 years.

Earlier today we were thinking, “Where do I go with my party hangover?” Read… Mortgage and HELOC balances, delinquencies, and foreclosures: How do drunk sailors hold up?

Enjoy reading and supporting Wolf Street? You can donate. I appreciate it very much. Click on the beer and iced tea mugs to see how:

Would you like to receive email notifications when new articles are published on WOLFSTREET? Sign up here.

![]()