China’s $680 billion external credit market has entered the least turbulent period since the real estate crisis unfolded two years ago, if only for the dwindling pool of surviving borrowers who have yet to default.

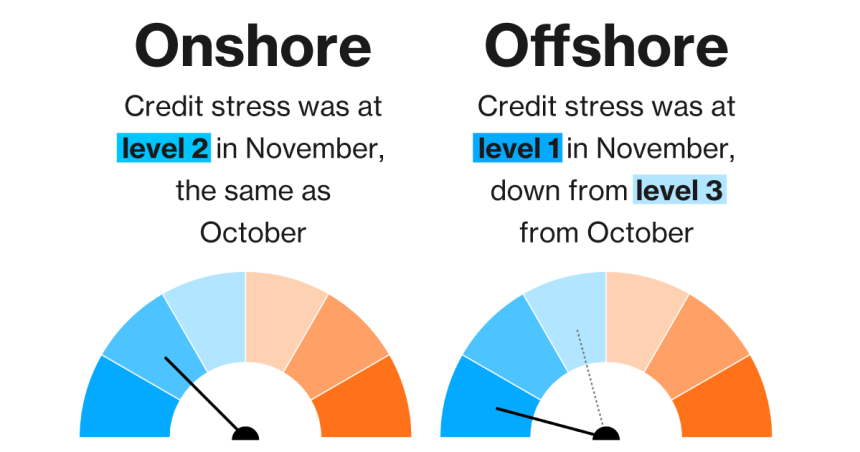

The market stress level fell to Level 1 last month from 3 in October, according to Bloomberg’s China Credit Tracker, the lowest level since data collection began in May 2021. The scale indicates rising degrees of financial stress across a range of 1 to 6.

The index remained at level 2 for the country’s domestic corporate bond market.

This rare calm among global investors offers an early sign of relief after Beijing stepped up a campaign to prevent a prolonged housing market slump and industry-wide liquidity pressure from undermining financial stability. Policy support has accelerated in the past month, from providing financing for a potential list of 50 developers, to an unprecedented proposal to allow banks to provide unsecured loans to eligible construction companies.

However, as major defaulters, from China Evergrande Group to Country Garden Holdings, continue to impose distress on creditors and generate uncertainty over debt restructuring, how long the calm can last remains in question.

Anna Chang, a credit analyst at T Rowe Price Hong Kong Ltd, said the authorities’ recent rescue steps “indicate the government’s efforts to limit the downside.” Greater chance of survival.”

The decline in tensions abroad came as Chinese junk dollar bonds, dominated by the country’s cash-strapped construction companies, have risen for three straight months, a Bloomberg index that excludes distressed debt shows. This is the best performance since January.

The dollar bills of the survivors of Agile Group Holdings Ltd. To Seazen Holdings Co., Ltd. And Ping An Real Estate Co., was among the best performers last month, with Agile leading the gains with total returns of more than 77%.

A Bloomberg Intelligence gauge of Chinese real estate stocks also rose 6% in November, ending a three-month decline.

In addition to moves aimed at improving financing conditions, authorities also made a rare offer of support for China Vanke, the country’s second-largest builder by sales, to ease concerns about payment risks that have led to a sell-off in its dollar bonds. .

Beijing, Guangdong have the most distressed local banknotes

Note: The map shows the local banknote market in mainland China. Source: Bloomberg

However, the housing sector’s road to recovery remains bumpy, as payment setbacks and debt uncertainties remain.

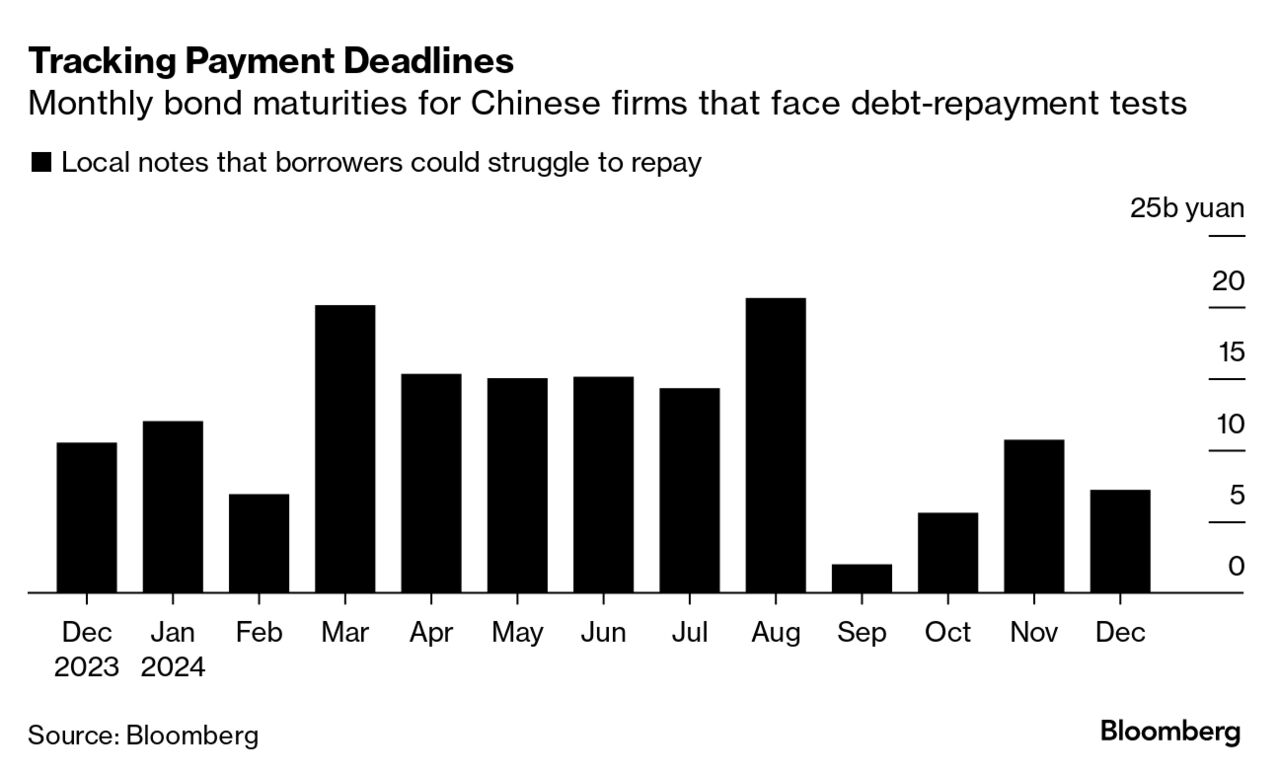

Track payment deadlines

Monthly bond maturities of Chinese companies facing debt repayment tests

Just last month, Shanghai-based Powerlong Real Estate Holdings Ltd. defaulted on one of its dollar bonds due to slowing sales and deteriorating liquidity. Meanwhile, Evergrande, the country’s most indebted developer, continues to struggle to submit a restructuring plan that could save itself from potential court-ordered liquidation.

“To restore confidence in the sector, it will require not only an improvement in financing conditions, but also a tangible recovery in contracted sales, which has remained weak,” said Thu Ha Chow, head of Asia fixed income at Robeco Group. “For the market to see a real recovery, it will require a strengthening economy which in turn will give greater confidence to consumers and investors.”