The Fed reported significantly weakening consumer credit with negative revisions as well.

Consumer credit report reviews

Key points to review

- Most reviews are not rolling, but this affects the totals.

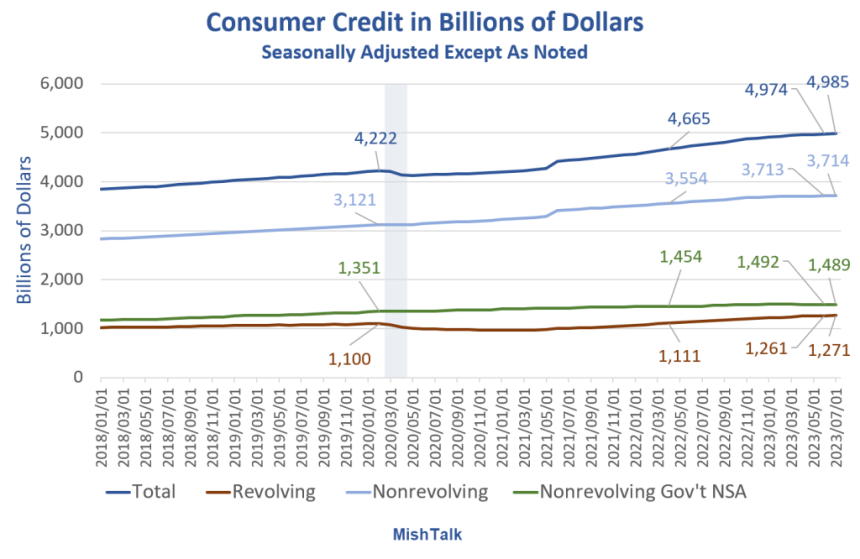

- Non-recurring credit increased by $1 billion in July Negative adjustment of $22 billion in June. The Federal Reserve revised the announced amount of $3.735 trillion to $3.713 trillion.

- In contrast, non-rotation affected the aggregates.

- Total credit rose $11 billion in July from Negative revision of $23 billion in June. The Fed revised the $4.997 trillion announced in June to $4.974 trillion.

Billions of dollars in non-revolving consumer credit

Implications of non-revolving credit

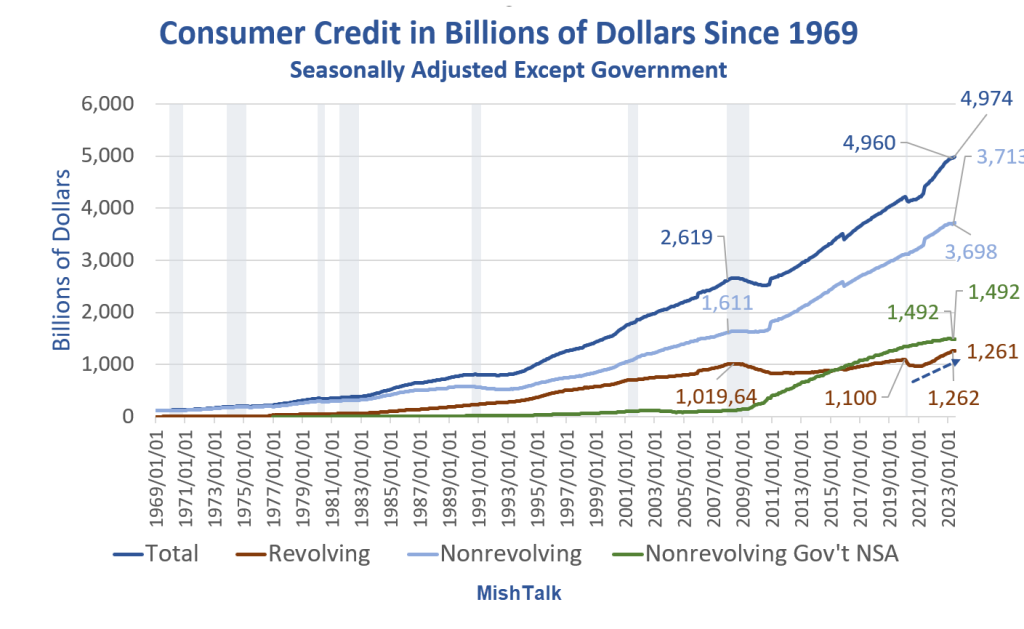

Assuming that the data is accurate (unlikely) or at least that the revision trend is accurate (likely), current mortgage and home sales data are questionable.

Real (inflation-adjusted) non-revolving credit peaked in June of 2021.

Billions of dollars in consumer credit since 1969

Consumers have generally done a pretty good job of avoiding credit card debt thanks to three rounds of fiscal stimulus.

However, inflation began to set in and the stimulus money was spent. The result is a sharp rise in credit card debt as shown by the blue arrow. Let’s focus on that.

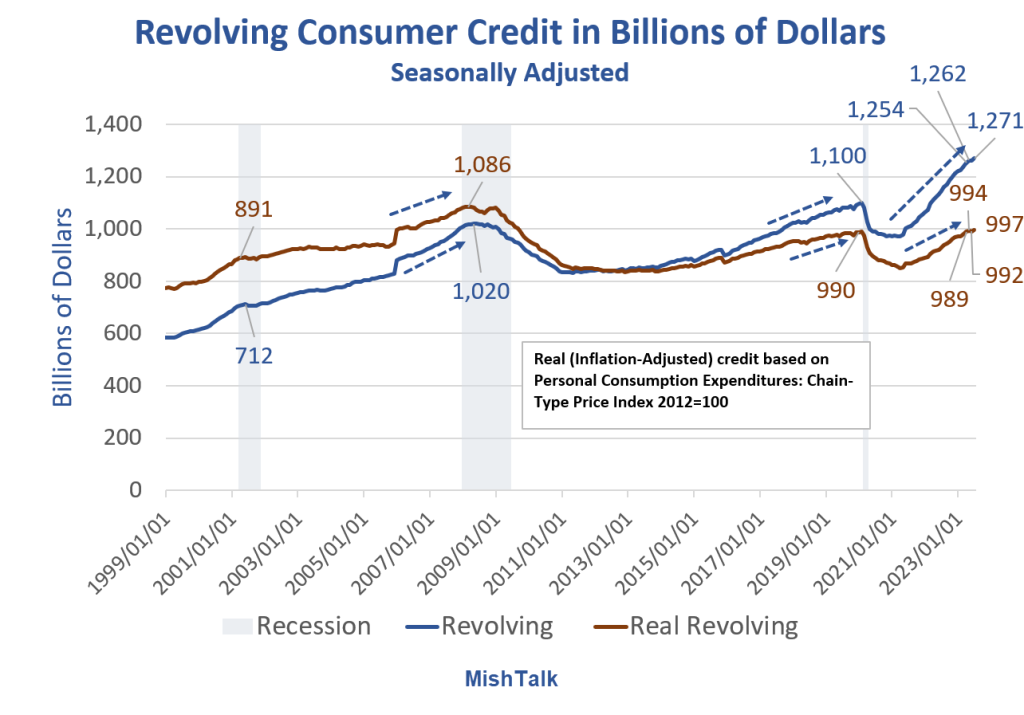

Billions of dollars in revolving consumer credit

A stunning decline in the accumulation of credit card debt

The speed at which consumers are running into credit card debt is astonishing.

Lifestyles with high inflation rates are difficult to maintain unless wages continue to rise.

The BLS and the Fed believe that the rate of increase in inflation is declining. Let’s say The data is correct, and consumers are suffering anyway.

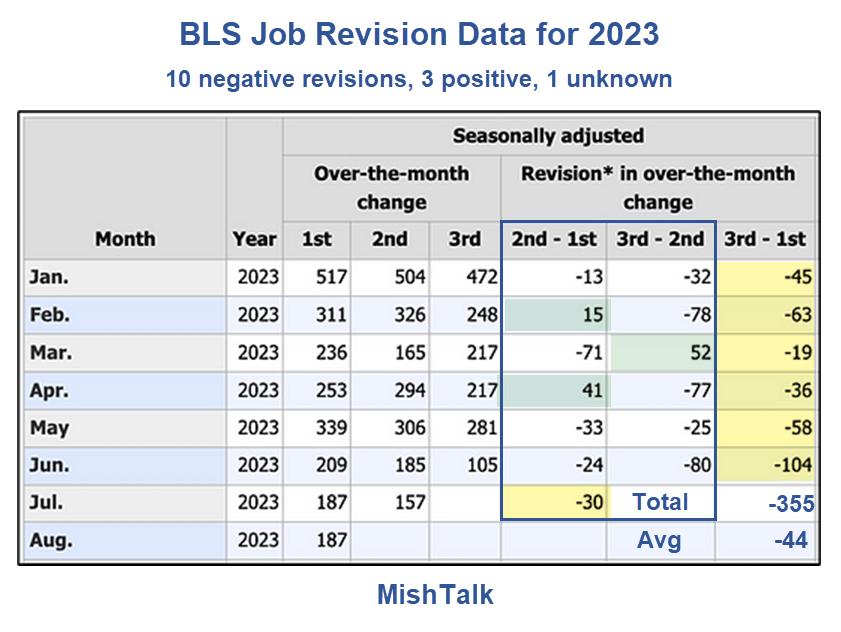

What happens if jobs decline?

This is actually the wrong question. Functional reviews (there’s that word again) have been overwhelmingly negative.

Jobs are still positive, assuming (there’s that word again) you believe the numbers and more negative reviews (there’s that word again) aren’t in play.

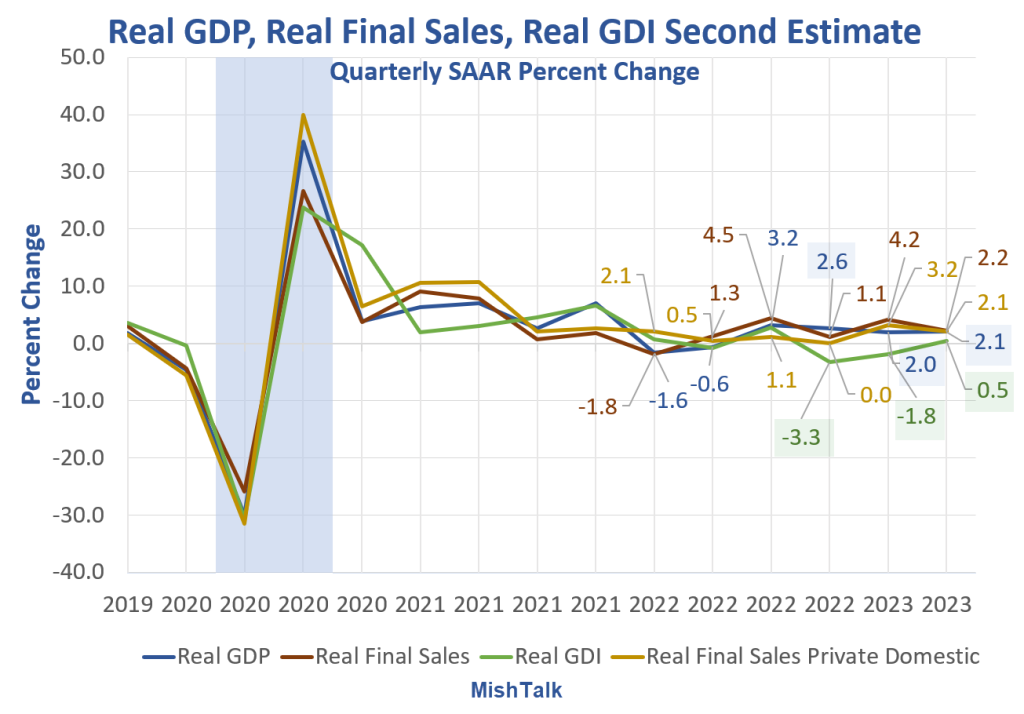

As long as you’re making assumptions, if you’re comfortable with the strength of Biden’s economy, it’s best to assume the GDP numbers are correct as well.

My assumption is that the GDP is completely wrong and that the Gross Domestic Income (GDI) numbers are much more likely to be correct than the GDP numbers. GDP and GDI are supposed to be the same, but they are not.

GDP vs. GDI

On August 30, it commented on the negative revision to Q2 GDP, and the significant discrepancy with GDI continues

If you’re a believer in GDP and jobs, you probably assume (there’s that word again) that GDP is accurate. The last three quarters are +2.6%, 2.0%, and 2.1%.

In contrast, the last three GDI metrics are -3.3%, -1.8%, and +0.5%, with the last quarter likely to be the most revised.

The Fed makes decisions on weak and inappropriate data that are frequently revised

I tied many of the ideas in this post together, in more detail (without the credit card reviews), in my previous post Fed Makes Decisions on Weak, Inappropriate Data and Reviews Too Frequently

Please give it a look. Meanwhile, damn the reviews, and have full faith in the future.