Image © Adobe Stock

Euro exchange rates are in focus over the remainder of the week as inflation readings are released from across Europe, starting with Germany and culminating with the eurozone-wide release on Friday.

Germany mentioned Headline inflation fell by 4.5% year-on-year in September, below analysts’ expectations of 4.6%, and a marked decline from 6.1% in August.

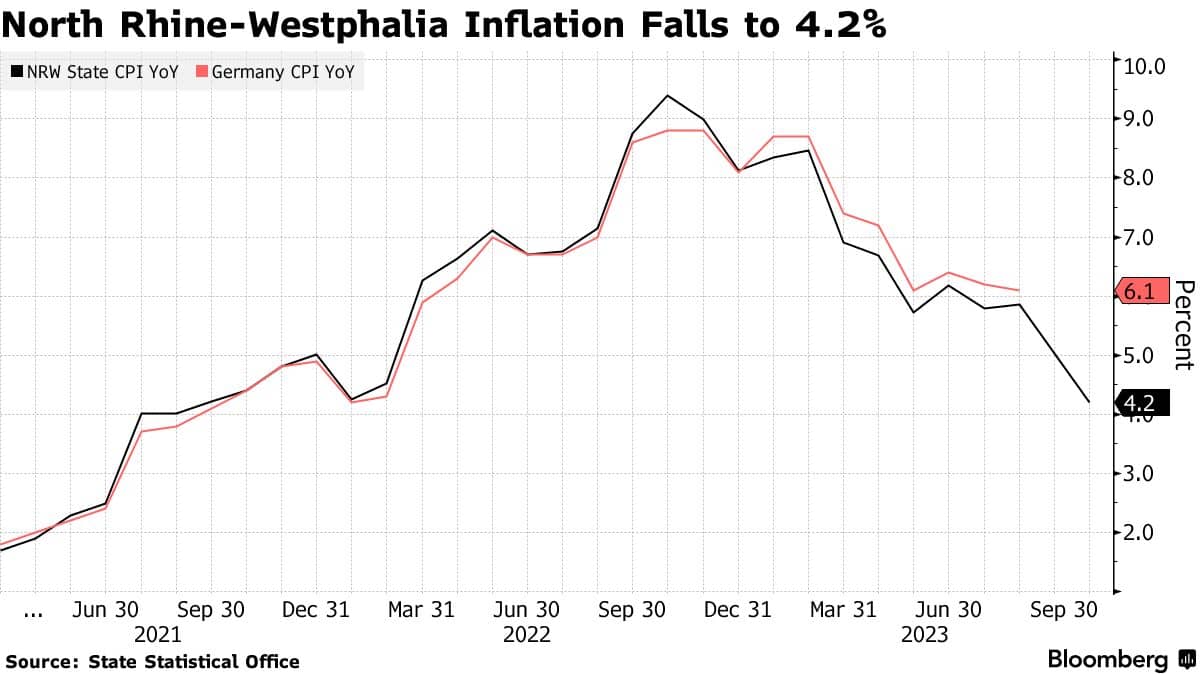

The move lower in the euro against the British pound and other currencies began earlier in the morning after inflation in the German state of North Rhine-Westphalia fell to 4.2% year-on-year in September from 5.8% in August, representing a significant decline in the inflation rate. The 5.9% the market was expecting raised expectations that the ECB had done enough by raising interest rates.

“CPI inflation data for German regions showed an easing in price pressures,” says Jane Foley, chief FX strategist at Rabobank. “This will support our internal view that the ECB has likely reached the top of its rate hike cycle.”

The North Rhine-Westphalia market region provides a good understanding of where the national figure is headed due to its large population and industrial base:

Image above courtesy of Bloomberg.

Other German states then reported lower-than-expected rates, with Bavaria’s year-on-year figure falling to 4.1% from 6.1% previously while coming in well below expectations of 5.9%. Hesse and Brandenburg also performed lower than expected.

However, the EUR/USD has risen to 1.0538 at the time of updating this article, but we should note a broader decline in the USD after a sharp rising pace that left it heavily overbought and deserving of a correction.

Alternatively, we can detect some distinct weakness in the Euro on the ‘crosses’: the Euro to Pound exchange rate fell another 0.30% on the day (on top of the previous day’s loss of 0.47%) at 0.8636. The British pound rose against the euro to 1.1580.

In fact, the euro is lower against all of its peers, along with the inflated dollar and the Canadian dollar.

Spain released its national figure of 3.5% year-on-year in September, which was in line with expectations, albeit slightly up from 2.6% in August.

Fuel costs will be the main driver of the rise making Spain’s core CPI reading more useful at -0.1% m/m, which would be seen as an across-the-board reflationary signal for the ECB. Spain is interesting as analysts note that the ‘pass-through’ of inflation is relatively fast, thus providing a peak into how Eurozone inflation trends will trend over the coming weeks.

“Core CPI fell in Spain (-0.1% m/m). The wheels are coming off the Eurozone inflation bus,” says Viraj Patel, a macroeconomist. “If demand continues to be weak, we will be talking about ECB cuts (not increases) in End of the year.” Strategist at Vanada Research.

Foreign exchange markets have now priced in the end of central banks’ interest rate hike cycles in major economies and are now fully focused on the potential for interest rate cuts in 2024. When and how strong these cuts begin will impact bond and currency markets.

If the market advances the timing of the ECB’s first cut – especially in relation to weak inflation dynamics – the euro could face difficulties.

The comprehensive Eurozone release is due on Friday, but what often happens is that the market response is usually complete by the time Germany and Spain release the numbers.

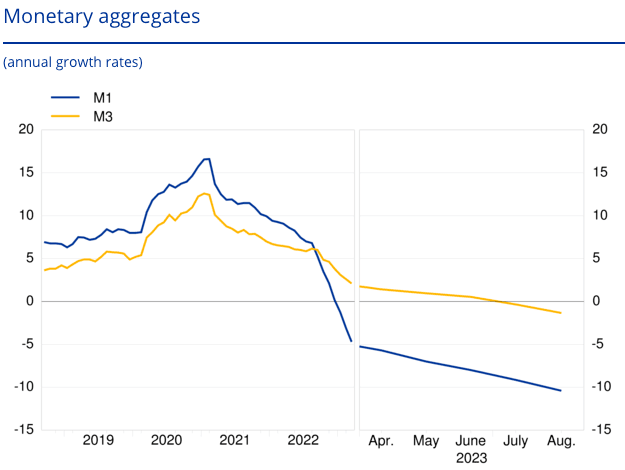

Low inflation rates are linked to key indicators pointing to deflationary dynamics including yesterday’s money supply data from the European Central Bank which showed a sharp decline:

Image courtesy of the European Central Bank.

The M3 money supply – a measure of the flow of money through the economy – fell by 1.3% year-on-year in August, indicating that the impact of interest rate hikes by the European Central Bank is being felt.

The consequences of a reduced money supply are weak demand and, ultimately, lower inflation.

“Annual M3 growth slowed from more than 12% in early 2021, and about 4% at the end of 2022, to -0.4% as of July. This reflects the impact of higher interest rates,” says Rhys Herbert, an economist at Harvard University. Lloyds Bank.

Such a contraction in the money supply and credit significantly weakens the region’s economic outlook, says Alex Kuptsikevich, chief market analyst at FxPro.

“In contrast to the United States, most loans in Europe are provided at floating interest rates, so an increase in the ECB’s key interest rate simultaneously tightens conditions for both new and existing loans. Thanks to this feature, the monetary policy transmission mechanism works faster “As a result, fewer interest rate increases are needed to cool the economy and, through it, inflation.”

The ECB may therefore find that it has tightened policy sufficiently.