TeamViewer expects €50 million in additional profits as Manchester United deal expires

Remote computer access company TeamViewer said it would save more than €50m (£43m) as Manchester United made plans to cancel its first sponsorship deal with the German company.

TeamViewer is initially set to be the club’s main sponsor until 2026.

But United said last night that it would end the sponsorship early to put chip maker Snapdragon on the front of its shirts instead from the start of next season, after revealing at the end of 2022 that it was looking for new partners.

This morning, TeamViewer said it expects the early termination of the deal to significantly boost its earnings. It expects to earn an additional €17.5 million in 2024, when its logo will appear on Manchester United shirts for half the calendar year, and an additional €35 million in 2025.

The company also indicated that it will continue to advertise on billboards at Old Trafford and the club’s digital channels.

TeamViewer shares rose 1.6% to €16.26 this morning in Frankfurt. It has risen by more than 60% in the past year.

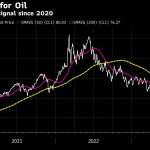

BP shares fell after the sudden departure of CEO Bernard Looney

BP shares came under pressure in morning trading after the oil major confirmed the departure of its CEO.

The company said in a statement today that Bernard Looney “has not been completely transparent” about “personal relationships with company colleagues.”

BP looked into anonymous allegations that Looney had what it called “a small number of historical relationships with colleagues before he became CEO” and found that there was “no violation of the company’s code of conduct.”

But after receiving “other allegations of a similar nature” recently, it found that Looney “did not provide details of all relationships.”

One of the best-known and best-paid chief executives on the FTSE 100, Looney’s shock departure comes after less than four years in the £10m-a-year job.

BP shares fell more than 6p to 516p, a drop of more than 1%.

Retail and consumer stocks fell as the FTSE 100 index fell after the economy contracted in July

London’s main stock market index fell again in early trading, with retail traders under pressure after economic data showed the economy contracted in July, as wet summer weather and higher interest rates cooled consumers.

Some big names have emerged from the high street and other major retailers. Ocado, the online grocery store, was the single biggest loser, down 18p to 783p. JD Sports was 2p softer at 138p.

Overall, the FTSE 100 fell 13 points to 7,514.70.

There were also notable declines for companies exposed to consumer spending on the FTSE 250. The mid-cap index is seen as more representative of the UK’s domestic economy. It fell 44 points to 18497.89. Domino’s Pizza lost 7p to 389p. JD Wetherspoon shares fell 7p to 693p.

A quick snapshot of the market as the pound falls further

The pound fell below US$1.25 according to the latest GDP figures, while the FTSE fell slightly.

Take a look at our full market snapshot

GDP decline ‘more than strikes and weather’

Paul Dales, chief UK economist at Capital Economics, said that while strikes and bad weather explain the hit to public sector and retail output, they do not explain all of the weak numbers.

“There is an underlying air of weakness,” he added. “This would make sense given that the dampening effect of higher interest rates should become more difficult now, and when other indicators, such as PMIs of activity, which exclude the drag on public sector activity from strikes, also point to a recession.

“This data suggests that Q3 GDP growth as a whole is likely to be well below the Bank of England’s +0.4% QoQ forecast. However, the strength of wage growth and steady core inflation (next update to this due next Wednesday) ) indicate to us that the bank will withdraw interest rates again at its policy meeting next Thursday.

Decrease in full year completion in Redrow

The cost of living and mortgage affordability crisis continues to negatively impact the housing market, builder Redrow said, as it revealed a decline in full-year completions.

The UK housebuilder, which has a main site in Colindale and focuses mainly on family homes predominantly in the south and south-east, completed 5,436 sales in the year to 2 July. This was 5% lower than the previous 12 months.

It managed to keep revenues steady at £2.13bn, but underlying profits before tax were 4% lower at £395m.

The industry has seen demand affected as the cost of living crisis and rising interest rates put increased pressure on buyers. The end of the Help to Buy program has also made affordability more difficult for some borrowers.

Noting that headwinds persist, Redrow said the sales market over the summer was tough, and sales per outlet during the first 10 weeks of the new financial year were 0.34, down from 0.61.

For the current financial year to July 2024, Redrow’s targeted revenue will range from £1.65bn to £1.7bn.

The FTSE 100 is expected to fall after the UK economy contracted in July

The FTSE 100 is expected to fall in the opening session, after gloomy July GDP data weighed on the mood.

The wider impact on the British economy of a rise in long-term interest rates by the Bank of England was a point of discussion as the value of all goods and services produced by the country in July fell by 0.5% from the previous month. This was the largest decline since December 2022. It was expected to fall by 0.2%. On a yearly basis, it’s been flat.

Spreadbetters expects the main stock market index in London to fall by about 30 points to 7,524 points. Similar declines in margins are expected on European exchanges.

A shallow recession is ‘increasingly likely’ with the UK economy shrinking by 0.5% in July

Jeremy Batstone-Carr, European strategist at Raymond James Investment Services, warned of the possibility of a recession after the latest GDP figures.

He said: “Today’s 0.5% fall in GDP provides further evidence that the resilience of the UK economy is beginning to diminish, and suggests that a shallow recession is increasingly likely over the remainder of the year.

“All sectors of the economy have started the third quarter under pressure, with the services and retail sectors particularly hard hit by unusual rains in July. Moreover, the delayed impact of previous interest rate increases is being felt across the economy. If banks continue to reduce… credit and withdraw lending, the economy will fail to gain any real momentum.The Bank of England should be cautious about further raising interest rates with this in mind.

Read more here

UK GDP shrinks by 0.5%

UK GDP fell by 0.5% in July, faster than expected, as bad weather hampered the economy.

The decline was widely expected, with economists predicting a 0.2% contraction in GDP.

The contraction, combined with early indicators pointing to further weakness in August, could put the UK on alert for a possible recession until the end of 2023, which is typically defined as successive quarters of GDP contraction.

Morning update: What you need to know to start the day

Good morning from the Evening Standard’s city desk.

The FTSE 100 unexpectedly lost one of its CEOs last night. News arrived in our inboxes just before 8pm that BP chief Bernard Looney had left the company due to “relations with colleagues”.

The oil giant said it investigated his past relationships with colleagues and initially found no violations of its code of conduct, but more allegations emerged, prompting Looney to admit he had not been completely transparent with the board.

Read the full story here.

On the other side of the pond, Apple finally bowed to pressure from the European Union and ditched the dedicated Lightning port on new iPhones in favor of the USB-C connection already used by Samsung and Google, which it admitted “has become a globally accepted standard.” See more major announcements from the US tech giant here.

Here’s a summary of our other top headlines from yesterday:

Today we expect results from Tullow Oil. In the US, in the afternoon we will get the full picture of Arm’s IPO price range before shares start trading tomorrow.

Bernard Looney has resigned as CEO of BP (Aaron Chown/PA)

/ Archives of the Palestinian Authority