via Metal miner

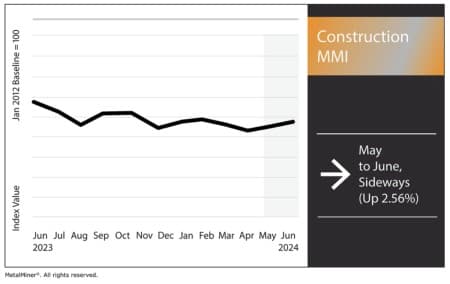

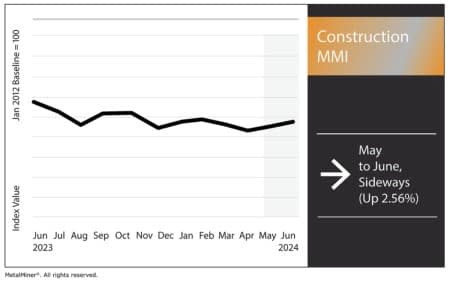

MMI construction (Monthly Metals Index) Continue to hold sideways on a monthly basis, without significant upward or downward pressure on industrial metals. Overall, the index saw a slight increase of 2.56% in price action. However, it failed to break out of the 10-month sideways price range. Weekly fuel surcharges decreased significantly, causing the index to decline. However, Chinese rebar saw a rise in prices, sending the index higher.

Once again, there was great pressure at home Both ways. Despite China’s slight recovery from a demand slowdown, orders remain fairly weak for industrial metals, which continues to impact the global construction industries.

China’s economy is sending shockwaves through global industrial metals markets

Demand for metals in China is still sluggish, which has a significant impact on the world’s industrial metal markets. According to multiple sources, there are several reasons behind the decline in demand.

First, the slowdown in China’s economic development has greatly affected industrial activity. In fact, the real estate sector, a major user of steel and other metals, continues to face declining investment and slowing construction activity. There will be a decline in demand for steel and other industrial metals as a direct result of this This contraction.

On the other hand, geopolitical tensions and rising interest rates have made matters worse. This is because global demand for metals declines when interest rates rise Economic concerns – Reducing investment and industrial production.

Handling incredible demand

Chinese manufacturers continue to turn to overseas markets to make up for domestic shortages, resulting in semi-finished and finished steel exports rising due to the country’s needs. Slow order. However, this change also increases the global glut, driving down costs. For example, aluminum prices continue to fall despite a general rise in industrial metal prices, mainly because China is not a member country. Strong buyer.

Optimism for growth in the US construction industry

Regarding the construction industry’s rise in the remainder of 2024, contractors remain confident. This optimism results from several factors. First, the market expects a significant increase in initiatives related to sustainable energy, transportation infrastructure and industry. There will likely be more investment and growth in these areas, which will increase demand for them Construction services And industrial minerals.

The sector is also well placed to benefit from government funding and assistance. Contractors expect a continuous flow of work with a focus on renewable energy and infrastructure modernization. This expected wave of projects will likely drive job growth, with some estimates suggesting the sector will need nearly 340,000 additional workers by the end of 2024 to keep up. With the request.

Reasons for doubt

However, there are still some reasons for doubts about the growth in the construction industry. The ongoing labor shortage is one of the major problems. Many companies point out that it is becoming increasingly difficult to find younger people with the right abilities, which can make it difficult for the sector to realize a project. Goals.

Furthermore, the overall mixed market picture indicates potential volatility. Contractors continue to prepare for potential changes in demand, which may lead to a slowdown in growth and activity Periods. There are also serious concerns due to some economic uncertainties, such as fluctuations in material prices and supply chain disruptions due to geopolitical conflicts.

Written by Jennifer Curry

More best reads from Oilprice.com: