Late last month, I wrote an article explaining why some say the economy isn’t doing as well under the Biden administration. For left-wing intellectuals, Biden’s failures to reform the labor market (such as passing the PRO Act) and welfare state reforms (such as passing Build Back Better) are reason enough for disappointment. For ordinary people, the relaxation of the welfare state due to the coronavirus and inflation have reduced real incomes for most people.

There were many reactions to the latter change in real income.

The most common responses were recognizing that the coronavirus welfare state will always be temporary, that inflation is out of Biden’s control, or that it’s worth taking the risk as part of ensuring sufficient total capital. The idea was that people shouldn’t get angry because they should. request. While this reaction may have some merit, many have argued that “people should better understand why their economic situation is worsening.” This is different from the claim that “people’s economic situation has not worsened.”

Another response I got was that we should expand our analysis beyond inflation-adjusted income and look specifically at wealth. This is a valid point. Income, as measured by the Current Population Survey, is not the only quantity associated with economic well-being.For example, the fact that Ten million The removal of people from Medicaid as part of COVID-19 relief isn’t captured well in the chart above, but the welfare state certainly isn’t great for those experiencing it.

People who talk about wealth tend to point out the following points: 2022 Consumer Finance Survey, was released in recent months and received a lot of press, especially in the “everything is great” variety. The problem with this report is that the SCF is conducted once every three years. So at best with this data, he can only compare 2022 with 2019.

Wealth increased from 2019 to 2022 (more on this later), but this may be because wealth increased significantly in 2020 and 2021, while wealth decreased in 2022 and recently. there is. After all, this is what happened to the income. If that’s what’s happening with wealth, it’s no wonder people are a little disappointed with our most recent experience with the economy.

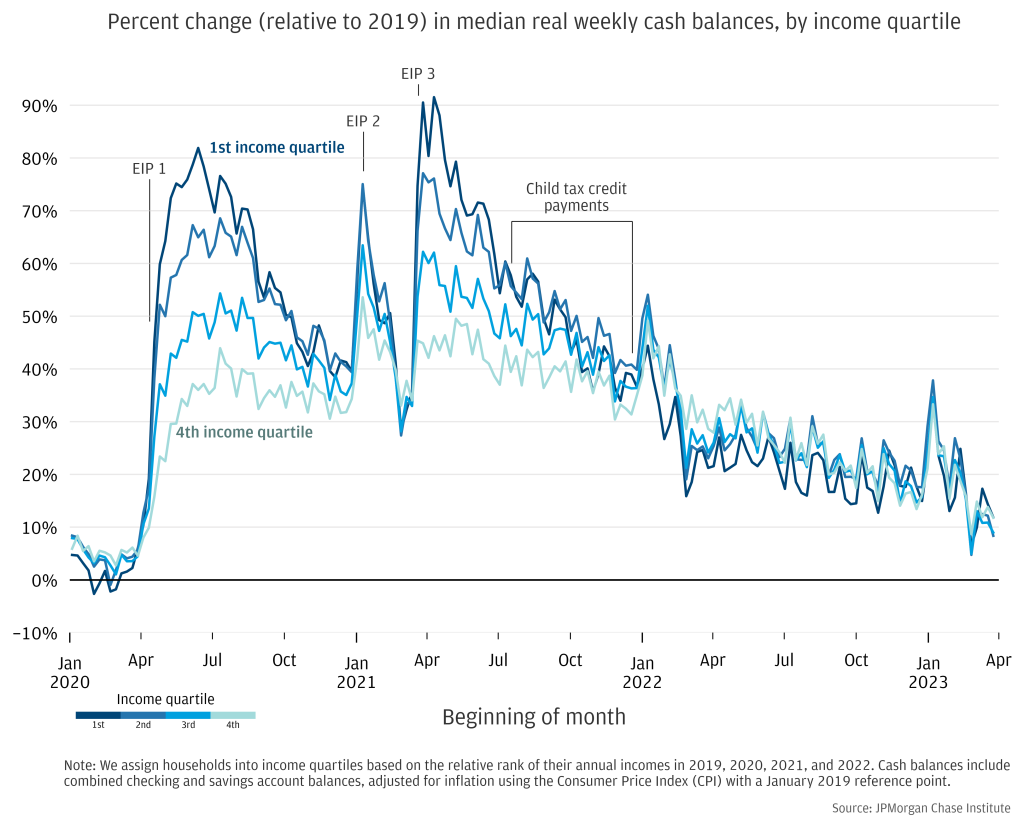

One indicator that this has happened with respect to wealth, particularly as it relates to day-to-day finances, is that: bank account data Published by JP Morgan.

This data shows that checking and savings account balances have increased in tandem with the coronavirus welfare state (EIP refers to stimulus checks). It reached its highest level in early 2021 and has been steadily declining ever since. Fair or not, seeing your cash balance drop by 40% at the same time as your income plummets due to welfare cuts and inflation can leave you dissatisfied with your personal finances.

Regarding the SCF data, it is not as clear-cut as it may seem at first glance. Between 2019 and 2022, the median wealth of the median quintile increased by $54,406.

SCF has 42 different categories The total assets and liabilities included in a family’s net worth. During this period, assets in the middle quintile increased by $72,075 (132% of net worth growth) and debt increased by $17,699 (-32% of net worth growth).

There are many ways to subdivide these various categories, but no matter how you do it, the story is the same. Wealth growth is overwhelmingly driven by inflation in used homes and used cars. During this period, the average price of a primary residence increased by $47,459 in the median quintile. The average price of a vehicle increased by $6,358. Together, the growth in the value of primary homes and cars accounted for 99% of the increase in net worth for the median quintile.

Of course, primary homes and vehicles often come with secured debt. Taking these into account, we find that primary home and auto assets account for $40,194 (or 74%) of the increase in median quintile net worth.

The findings are consistent with price indexes that show prices for used homes and cars soared more than 40 percent between 2019 and 2022.

Rising prices for used cars and homes are a real change in net worth, but they don’t do much for ordinary people who need a home and a car to make a living. People with second homes and cars may sell those assets to take advantage of capital gains from inflation. But that’s not something that less wealthy people generally have.

Rising home and car prices are clearly a negative impact for first-time home buyers or those looking to replace a worn-out car.

On average, current homeowners looking to replace their home find that rising home prices aren’t a big deal, but rising interest rates mean their monthly mortgage payments will be lower, even if they move into the same home. This means that it will be much more expensive.

Home value increases may be properly accessed through things like home equity loans and home equity lines of credit.However, the interest rates on these financial products are now excessively 9%, so leveraging household values in consumption in this way is no longer as viable as it once was.

In other words, wealth statistics do not indicate that the economic situation of ordinary people has improved significantly. Looking at metrics over the past few years, it’s particularly noticeable that cash balances have been declining rapidly.