All investors participate in the game of finding “growth winners” in the stock market. Last year, it was clear that AI-focused technologies were leading the bull market. Now Bernstein analyst Peter Weed has shifted his focus to 2024 and sees opportunities in several areas. cyber security stocks.

Weed acknowledged that while the cybersecurity sector is facing headwinds, it hasn’t affected the larger tech scene. Rapidly evolving online and digital threats, combined with the fast pace of innovation in this space, are making it difficult for businesses to gain traction. But some companies are doing so, and Weed explains why those companies are likely to continue to grow.

“All of the newly targeted companies are looking to leverage their customer segment advantages in network security and are developing application and cloud workload protection products, many of which are already shipping. ),” Weed wrote. Given the advantages of our new target vendors in their respective customer profiles, we believe they are strategically positioned as platform vendors that extend network protection from the starting point. ”

Bernstein analysts identify three specific cybersecurity stocks that investors should buy. TipRank Database To find out what Wall Street thinks of them. Let’s take a closer look.

Z scaler (ZS)

First on the list is network security specialist Zscaler. The company operates through a cloud-native platform called Zero Trust Exchange, which provides the ability to securely connect apps, devices, and users on any type of customer network. This ability to create secure digital connections builds trust by increasing user confidence and driving business productivity. Zero Trust exchanges operate at different levels, including user-to-app, app-to-app, and machine-to-machine connections.

Building trust is no easy task, as evidenced by some of the numbers the company can justly be proud of. Zscaler’s platform monitors more than 360 billion transactions every day and prevents more than 9 billion security incidents and policy violations each day. Collectively, the company’s platforms process more than 500 trillion signals every day that are essential to the cloud effect of AI and machine learning.

Zscaler prides itself on the capabilities of its platform and products, and its customers are happy with the results. These include reports of an 80% faster user experience, a 70% reduction in digital infrastructure costs, and a 35x reduction in the number of infected machines. These results come from Zscaler’s ability to eliminate threats, simplify and ensure secure access, and automate the entire process. The company does this at scale, with approximately 7,700 customers totaling more than 41 million regular platform users.

The company’s latest financial results, reported in November for the first quarter of fiscal 2024 (October quarter), showed continued growth in multiple areas. The company’s top profit came in at $496.7 million, an increase of nearly 40% year over year and $23.27 million more than expected. Ultimately, Zscaler reported his non-GAAP earnings per share of 67 cents. This was up from 29 cents a year earlier and beat expectations by 18 cents. At the end of the quarter, Zscaler had $2.3 billion in cash and liquid assets.

In several other key metrics, Zscaler reported a total of 2,708 customers with annual recurring revenue (ARR) above $100,000, with 468 customers having ARR above $1 million. These total customer counts increased 22% and 34% year-over-year, respectively.

For Weed, the key takeaway here is Zscaler’s strong position in the sector and solid opportunities for strong growth going forward. He writes: “ZScaler’s SSE (Security Services Edge) products are tailored for large organizations that are cloud native or are moving to the cloud. There is little difference between the SSE needs of traditional on-premises organizations. Given its powerful SWG and ZTNA services, we expect ZScaler to dominate the SSE market. ZScaler has PoPs (Points of Presence) worldwide , and its cloud delivery services are highly scalable, given that SSE is an early technology architecture and ZScaler is well-positioned to serve any customer adopting the cloud. We are looking at a long growth runway. Our core SSE product has grown at ~30% CAGR over the last decade, with other products built around cloud security also growing at mid-30% CAGR. We expect it to grow at a CAGR.”

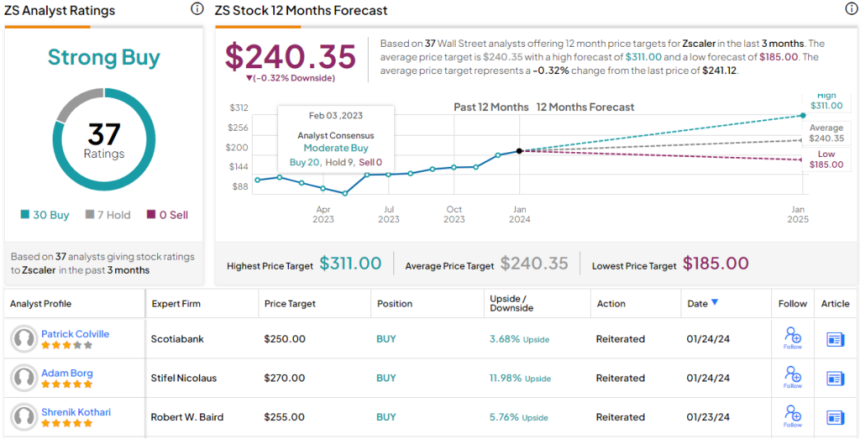

Bernstein analysts also rate these stocks as Outperform (Buy), and their $311 price target suggests 29% upside potential in one year. (To see Weed’s track record, click here)

Wall Street gives the stock a consensus rating of Strong Buy based on 37 recent analyst reviews (including 30 Buys and 7 Holds). That said, the average price target of $240.35 suggests the stock will remain range-bound for now. (look Zscaler stock price prediction)

sentinel one (S)

Next on Bernstein’s list of picks is SentinelOne, a company with a cybersecurity platform aimed at protecting the digital infrastructure essential to network systems. SentinelOne focuses on protecting data systems and their associated information, processing and storage subsystems, using AI-based solutions to enable autonomous early detection and response to threats.

AI is a “value-add” in SentinelOne’s product offering and is used to attract customers. What this means in practice is that the company’s endpoint security platform uses machine learning to better monitor any device, including PCs, IoT devices, tablets, smartphones, wearables, medical devices, and “smart” digital printers. It means you’re constantly learning how to do things. It is connected to a network and operates to send or receive information.

SentinelOne’s particular focus on endpoint security is an important aspect of cybersecurity. These devices are one of the most common entry points for digital threats (think computer viruses, malware, phishing scams, etc. on laptops and smartphones), and SentinelOne’s systems are actively trying to attack them. It works. And stop these threats.

A look at SentinelOne’s last earnings release, Q3 FY24 (October quarter), shows that the company beat expectations on both revenue and revenue. The company’s revenue was $164.2 million, or $7.85 million better than expected, and its bottom line, reported as a non-GAAP EPS loss of 3 cents per share, was a penny better than expected.

SentinelOne also reported strong ARR numbers, an important indicator for future growth. The figure was up to $669.3 million, an increase of 43% year over year. The company ended its fiscal third quarter with a total of more than 11,500 customers, 1,060 of whom had an ARR of more than $100,000 each.

We checked back with Peter Weed and found that the analyst is optimistic about SentinelOne and is cautious about the company’s ability to modernize its product line as well as diversify its product applicability to capitalize on further growth. I see that you are quoting. He writes: “SentinelOne has a strong presence in the SMB market. In addition to solutions delivered in the cloud, we also have on-premises versions of our solutions. Yet, we will be able to serve customers across all three modern areas. Additionally, as SentinelOne modernizes its endpoint protection systems, we will win in the highly fragmented SMB space. We expect further tailwinds. We expect SentinelOne to grow by up to 6x by 2030 as we are well-positioned to serve clients across the latest technology spectrum.”

Mr. Weed quantified his stance, rating S shares as “outperform (buy)” and setting a price target of $34, expressing confidence that the stock will rise 23% next year.

The “Moderate Buy” consensus rating on SentinelOne stock is based on a near-even split among 27 recent analyst reviews (14 buys and 13 holds). But again, the average target price of $27.41 here means the stock is currently well valued. (look SentinelOne stock price prediction)

crowdstrike holdings (CRWD)

Rounding out the Bernstein Recommended list is CrowdStrike, a top-rated cybersecurity company for endpoint security, identity threat detection, and ransomware protection. The company’s Falcon Endpoint Protection platform is well-known and highly regarded, encompassing a suite of products that have helped establish industry standards in cloud-based security modules, digital security, and online network protection. The company makes its products and platform available through a popular SaaS subscription model.

CrowdStrike uses AI technology to classify large amounts of security data to increase platform effectiveness and provide faster threat visibility. Faster detection means faster neutralization, simplifying your security environment. This makes CrownStrike’s systems a single agent against breaches, ransomware, and other cyber-based attacks, providing maximum protection from day one of installation.

The company gives customers three reasons to switch to Falcon products. These are the values of better threat protection, better security performance, and a better security budget. The latter is an important point that is often lost in the shuffle, but in digital security and network protection, it is always cheaper to prevent a major incident than to clean up a server after the fact. is a fact.

CRWD stock has performed well over the past 12 months, rising 184% and far outperforming the broader market. The company’s performance was also supported by a strong latest financial release for the third quarter of 2024 (October period). CrowdStrike reported that sales were $786 million, up 35.3% year over year and $8.62 million higher than expected. The bottom line, reported on a non-GAAP basis at 82 cents per diluted share, was more than double the year-ago period’s result of 40 cents and beat expectations by 8 cents. The company’s ARR increased 35% year over year in the quarter, reaching $3.15 billion, passing the $3 billion milestone. Overall, it was an impressive performance.

And analyst Peter Weed was also impressed. Bernstein’s cyber experts approve of his CRWD. Weed likes the company’s cloud-first direction and the potential for further expansion. “CrowdStrike’s Endpoint Protection Platform (EPP) products are delivered in the cloud and are relevant and equally effective regardless of a customer’s IT architecture. However, because CrowdStrike’s services are delivered in the cloud, they typically Adopted by cloud-first organizations, this gives CrowdStrike a natural right to win in two areas of modern IT architecture.Additionally, CrowdStrike will further expand into new avenues of growth, such as next-generation SIEM products. We continue to be selective about our products moving forward. Therefore, we believe that the growth of our EPP products will allow us to continue to grow in the mid-$20s this decade.”

In the case of Weed, this translates into an even Outperform (Buy) rating. His price target for CRWD is $334, implying a nearly 11% annual price upside. (To see Weed’s track record, click here)

Overall, CrowdStrike’s stock has a consensus rating of “Strong Buy”, with 40 analyst reviews out of which 38 are rated “buy” and 2 are rated “hold”. It has become. However, a significant increase in stock price pushed the stock price up to $301.35. This is slightly above the average target price of $296.68. (look CrowdStrike stock price prediction)

Visit TipRanks to find good ideas for trading stocks at attractive valuations. best stocks to buya tool that unites all of TipRanks’ stock insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. Content is for informational purposes only. It is very important to perform your own analysis before making any investment.