In theory, governments can finance their spending in three ways. First, it can raise revenue through taxes, such as personal income taxes and corporate taxes. Second, it can borrow from the public. Third, it can simply print money.

The revenue raised by printing money is called seigniorage, which is the difference between the cost of printing money and the value of the money when it is in the financial system.

- Nigeria approaches its bandwidth in all three ways. Tax collection was terrible. Nigeria has one of the lowest tax collection rates in the world at about 10.8 percent of GDP. Muhammadu Buhari left debts worth 77 trillion naira ($167 billion) to local and foreign creditors.

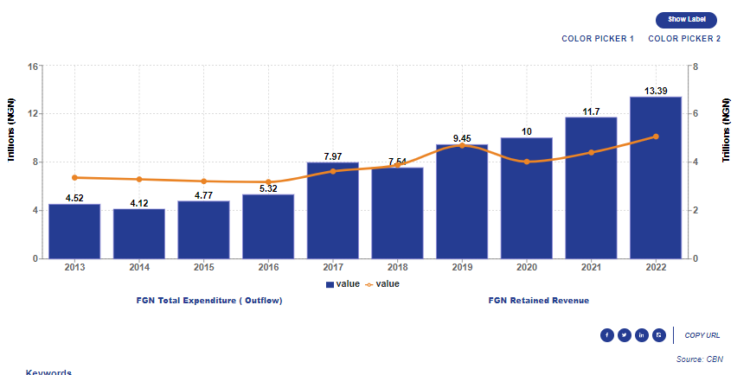

- Already, 96% of government revenues are used to service debt, and there have been concerns that the government’s cash crunch could worsen if additional revenues are not generated.

- The third measure, printing money, is economically unpopular because inflation exceeds 26.72% as a result of the central bank through the monetary phenomenon of illegally financing the massive deficit of the federal government to the tune of 23 trillion naira, through lending methods and means.

- Therefore, the Central Bank of Nigeria must move towards eliminating excess liquidity.

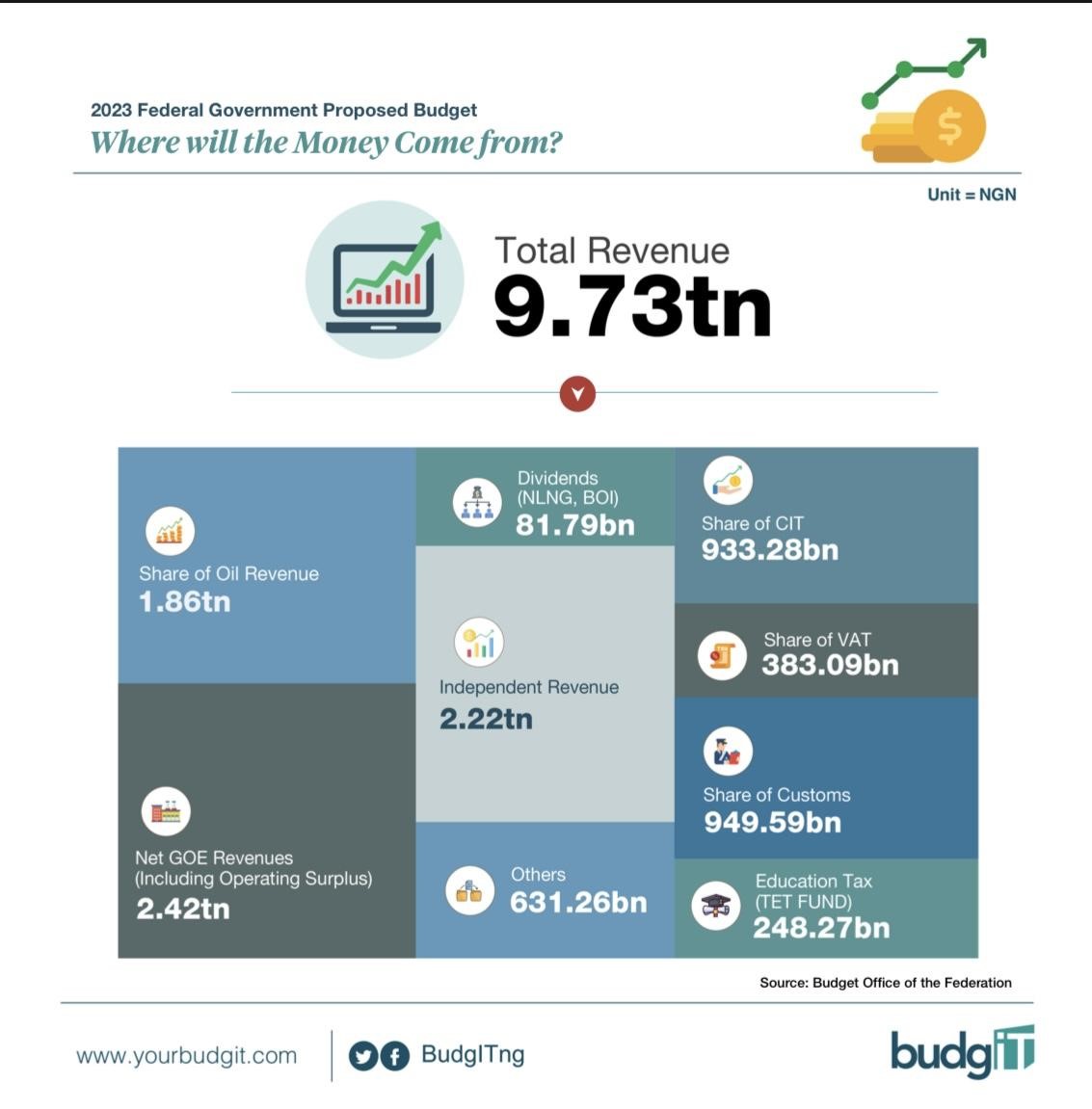

In addition, only 47% of the 2023 budget will be funded from revenues. The other part – borrowing. The budget composition is also not inspiring.

1. The cost of debt servicing, amounting to about 6 trillion naira, represents about 31% of the budget. This underscores the need for urgent action to address poor revenue performance and spending efficiency.

2. Non-debt-related recurrent expenditure (NDRE) of N8.27 trillion remains the largest expenditure in the budget (about 40%). It includes staff cost of 4.99 trillion. This is a problem – a quarter of the country’s budget spent on less than a million of the country’s population seems a bit shocking especially since government employees are not transparent, accountable and efficient.

3. Total annual revenue estimated at 10.49 trillion naira ($13 billion) – Apple made more than just selling iPads ($23 billion) in 2023. Nigeria has one of the lowest government revenues in the world

4. FG’s share of oil revenues was 1.86 trillion naira, less than $2-4 billion depending on the exchange rate you use. But our politicians live lifestyles like the ones we achieved in 2022 when we generated $161 billion in net oil income for Saudi Aramco.

5. Debt service and expenses rise but revenues do not.

Nigeria is an oil producing country, but many of its citizens are yet to accept the cold fact that its oil revenues are incapable of developing the country.

As of today, there has been only a partial recovery in oil production, to 1.57 million barrels per day (including condensate) in September from a low of 1.25 million barrels per day in September 2022, and a moderate increase expected in 2024-2025, with an average of 1.81 million barrels per day, aided by improved onshore monitoring.

However, this is still well below the 2.09 million bpd in 2019, reflecting chronic underinvestment in the sector, and the potential for ongoing production outages.

Overall, we have not been able to reach 2.5 million barrels per day – our assumed production capacity, but Nigeria’s population has risen as shown in the chart below, while oil production has declined over the past 20 years.

Therefore, we are facing a difficult situation, where the oil is not working at full capacity but the country’s population is growing larger.

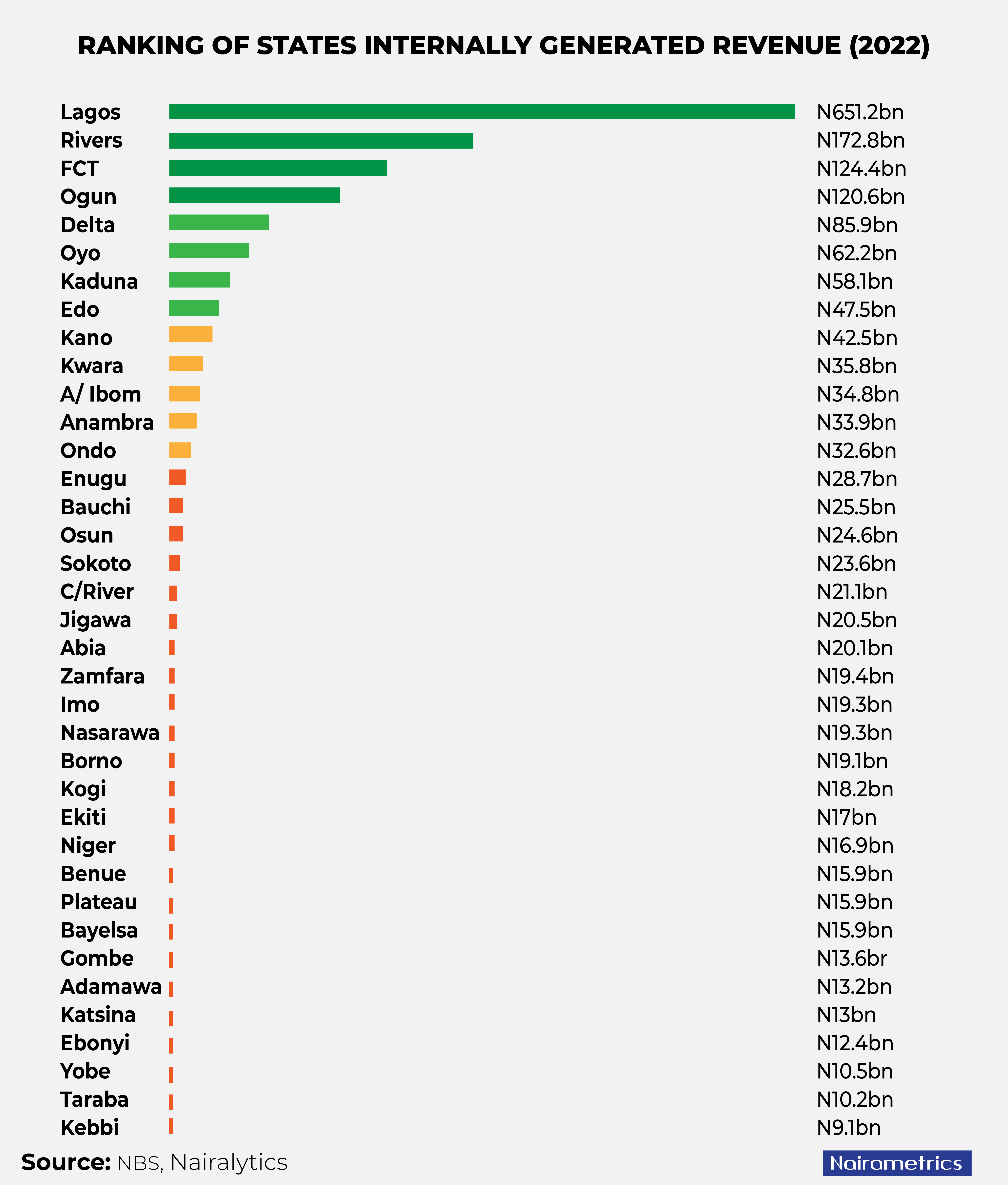

Financially, sub-nationals are not doing well either. State governors are not innovative in their revenue generation capabilities.

There is nothing left after they pay salaries and cut some roads. Most of the countries are not economically viable and are highly dependent on FAAC.

Interestingly, they are now embarking on white elephant projects and building airports that they cannot operate – which is draining FAAN’s resources.

The truth is that Nigeria does not have the necessary financial framework to ensure prosperity for some 200 million Nigerians. There is a note from the World Bank about our weak spending levels.

- “To boost economic development, Nigeria needs to increase its spending from its current very low levels.

- Despite its enormous development needs, Nigeria spends only $220 per Nigerian annually, at only 12% of GDP, one of the lowest levels of spending in the world.

- Unfortunately, low public spending translates into poor development results. The country is among the eight economies with the lowest human capital in the world, and is ranked 167th out of 174 countries on the World Bank’s Human Capital Index.

- As a result, a child born in Nigeria today will only be 36% less productive when he grows up than he would have been if he had access to effective education and health services.

- In addition, infrastructure needs remain very high: to provide all the infrastructure the economy needs to maximize its potential, the country will need to invest $3 trillion by 2050.

These numbers don’t look great. Mathematics is not mathematics. Something must be done. Something has to change. The country is on the brink – and the uproar and conflict over the 2023 presidential election is understandable.

Financially, the top three candidates had precedents that guided their fiscal ideologies. For the current president, his predecessors relied on taxes and bold fiscal reforms.

The runner-up, Atiku Abubakar, is pro-capitalism and a supporter of restructuring to give countries more power and resources to achieve better outcomes for their people.

Peter Obi, who came in third place, was keen on cost cutting measures, reducing high management costs and saving money/revenue.

He advocated saving surplus crude oil revenues a decade ago, which would have bailed out the country when macroeconomic shocks came.

All three have great ideas to salvage the country’s fiscal problem, but the debate will be on what should be a priority for Nigeria given our economic reality – should we grow national wealth (BAT), allow sub-nationals to grow their wealth (AA), or reduce how Government spending of current national wealth.

This is the question that should be at the forefront of our political discussions.

My expectations;

For the president and his team, my expectations are:

- A) Improving tax collection and taxes on GDP. The findings of the Presidential Commission on Fiscal Policy and Tax Reforms are of great importance. The committee is chaired by former PWC partner Taiwo Oyedele, who once said Nigeria had the potential to generate 40 trillion naira in tax revenue (four times higher than current tax income).

- b) Unleash the potential of Nigeria’s oil and gas to attract more foreign exchange inflows, revenues and investments

- C) Eliminate oil subsidies that cost $10 billion in 2022, an expectation he fulfilled.

- d) Support devaluation/foreign exchange adjustments to reduce dollar wastage – which met expectations.

- e) Reinvest subsidy savings and windfall income generated by the depreciation of the naira to grow new funds

As for the central bank governor, my expectations are:

- A) Inflation management and price stability.

- b) Achieving foreign exchange stability by expertly managing the floating exchange rate mechanism – will be reliance on foreign exchange flows and recognition of the link between inflation and foreign exchange fluctuations

- c) In cooperation with the financial side, clearing the backlog in the foreign exchange market and fostering an environment for the repatriation of dollar capital is crucial

- D) Restoring the transition between official interest rates and market rates.

Recommendations.

- The government must do everything in its power to gain the trust of its citizens. If people see that their taxes are spent wisely, they will be motivated to pay taxes. swap. No “yachts” and SUVs.

- After the permanent elimination of subsidies, stopping oil theft should be followed by improved tax compliance, taxpayer segmentation, customs modernization, and the adoption of customs duty and VAT rates similar to those prevailing in West African counterpart countries.

- The executive must also pay greater attention to promoting exports (which the weak currency supports) and supporting non-oil revenues. There must be a macroeconomic structural framework for new money to grow. Nigeria must ask itself one question: What can we produce for the world, similar to how Taiwan produces semiconductors?

- Spending money on productive things – A direct consequence of the high cost of governance in Nigeria is that less than 30 percent of FGN’s resources have been available to finance capital projects since 2017 when the government set itself a minimum target of 30 percent. Even so, a large portion of this is for “management capital” and not core capital spending. Capital projects must bring in future revenues. Road and transit projects linking farms to markets should be a priority, and this should be circulated to state and local governments. Government decision-making should obey the time-tested rule of a democracy: do what gives the greatest benefit to the greatest number of people within the project site. As resources become scarce, you have to direct money to projects that provide returns on investment.

- Invest in agriculture – food prices must fall. Data indicate that Nigerians spend 60% of their income on food. For comparison, an American spends 10% of his income on food. This would be more acceptable.