After being exposed to inflation, incomes have now exceeded the inflation rate for the 17th consecutive month.

Written by Wolf Richter for WOLF STREET.

With incomes well above the rate of inflation, our “drunk sailors,” as we lovingly and mockingly called them, continued to increase their spending in May, and they did so at a steady pace, roughly consistent with the good times just before the pandemic, and they saved the rest, “our sailors Drunks,” and the savings rate also rose.

Disposable income, adjusted for inflationU.S. per capita income rose 0.5% in May from April, the largest increase since January 2023, the Bureau of Economic Analysis reported today. By contrast, in April, disposable income was barely keeping pace with inflation.

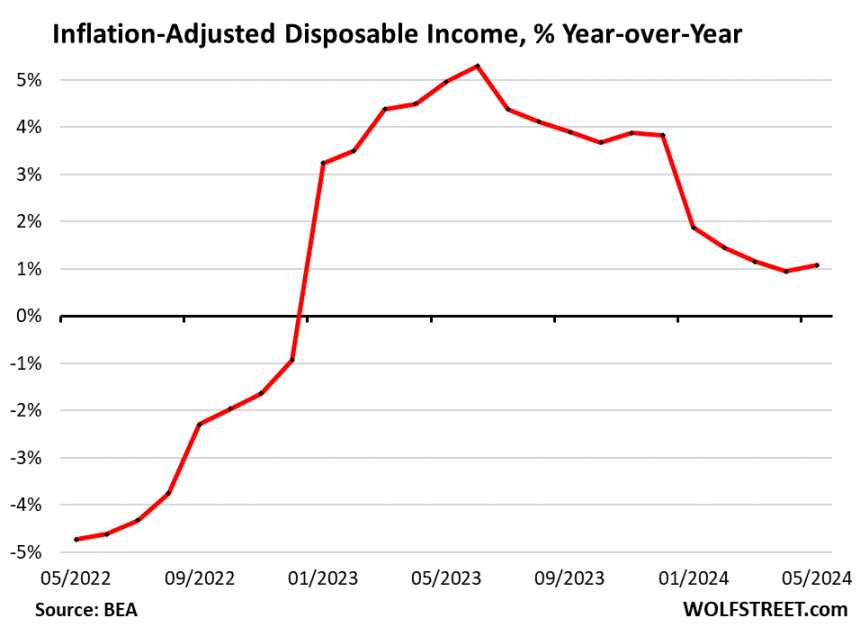

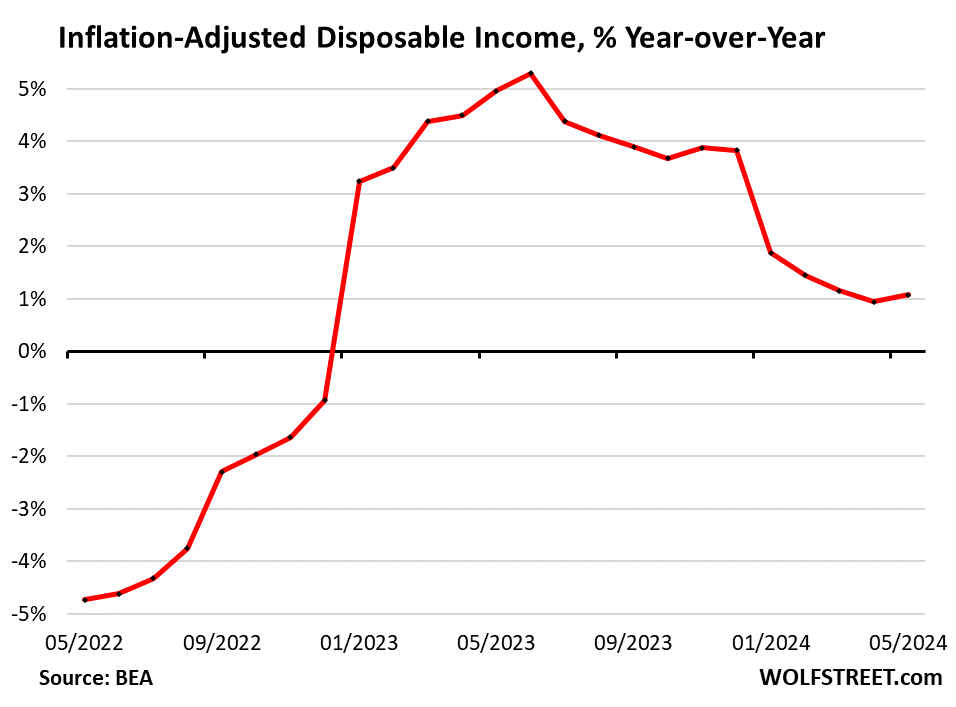

Compared to last year, inflation-adjusted disposable income increased by 1.1%. This marks the 17th straight month that disposable income has outpaced inflation on an annual basis, after taking a massive hit in 2021 through mid-2022, when the inflation explosion far outpaced lagging wage increases. But the growth rate of “real” incomes has slowed significantly from a range of 4% year-on-year in 2023 to about 1%. However, they outpace the inflation rate, and that is what matters.

Disposable income is income from all sources after income taxes and Social Security payments are deducted. It includes income from wages and salaries, transfer payments from the government (mostly Social Security benefits, but also Veterans Administration benefits, unemployment benefits, welfare benefits, etc.), and income from interest, dividends, rents, farms, personal businesses, etc. But it excludes capital gains. Disposable income is what consumers have left to spend on goods and services and to save. They have spent a lot and saved a lot, too.

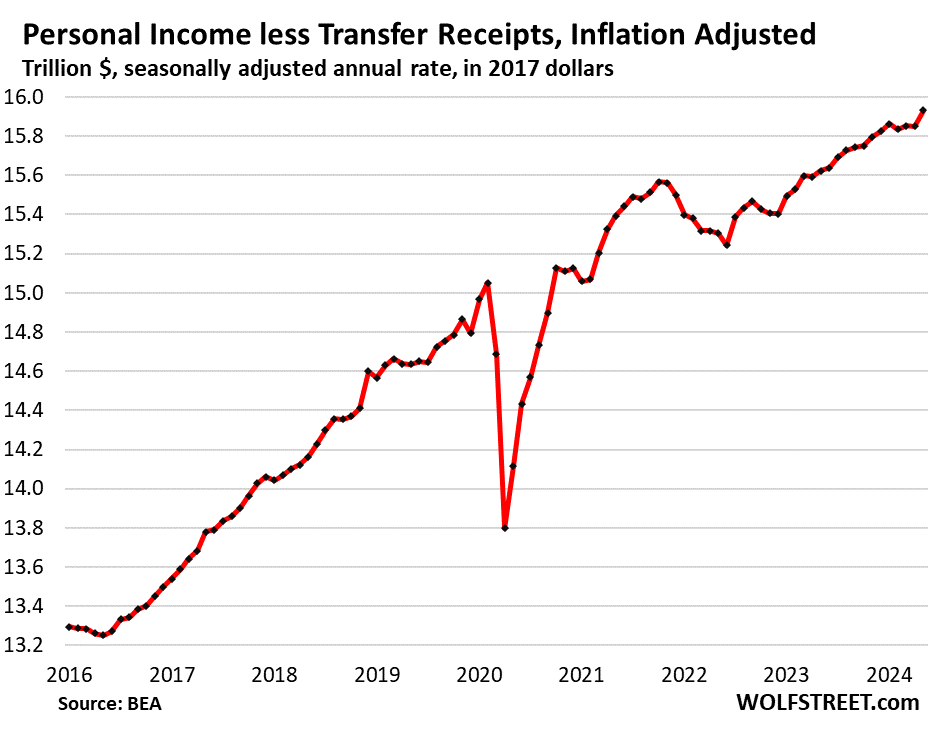

Personal income without Inflation-adjusted transfer receipts, It rose 0.5% in May compared to April, or an annualized rate of $81 billion, and 2.0% year over year. This means that our drunken sailors have outpaced inflation by a fairly large margin, having taken a beating in 2021 through mid-2022.

This income is from wages, interest, dividends, rental properties, farm income, small business income, etc.

This income growth is a function of employment growth, rising wages, rising dividend and interest incomes, rising rental incomes, and so on. Small landlords own about 11 million single-family rental homes, ranging from 1 to 9 rental homes, and for them, rental income is important.

Transfer receiptsTax revenues, adjusted for inflation, rose 0.3% in May from April, or an annual rate of $12 billion, and 1.9% year over year.

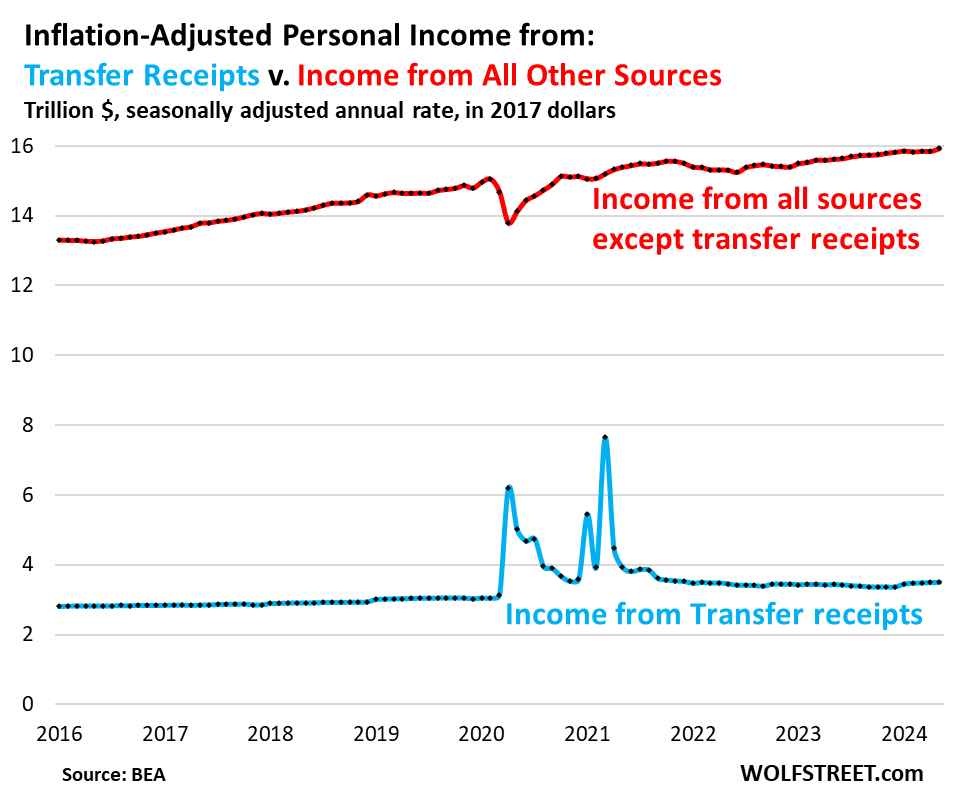

Transfer receipts are currently dominated by Social Security benefits that grow as more people receive them and the benefits increase. They also include VA benefits, unemployment benefits, welfare benefits, etc. But during the pandemic, they have been dominated by stimulus checks, unemployment benefits, supplemental unemployment benefits, and other pandemic payments to consumers (in blue in the chart below).

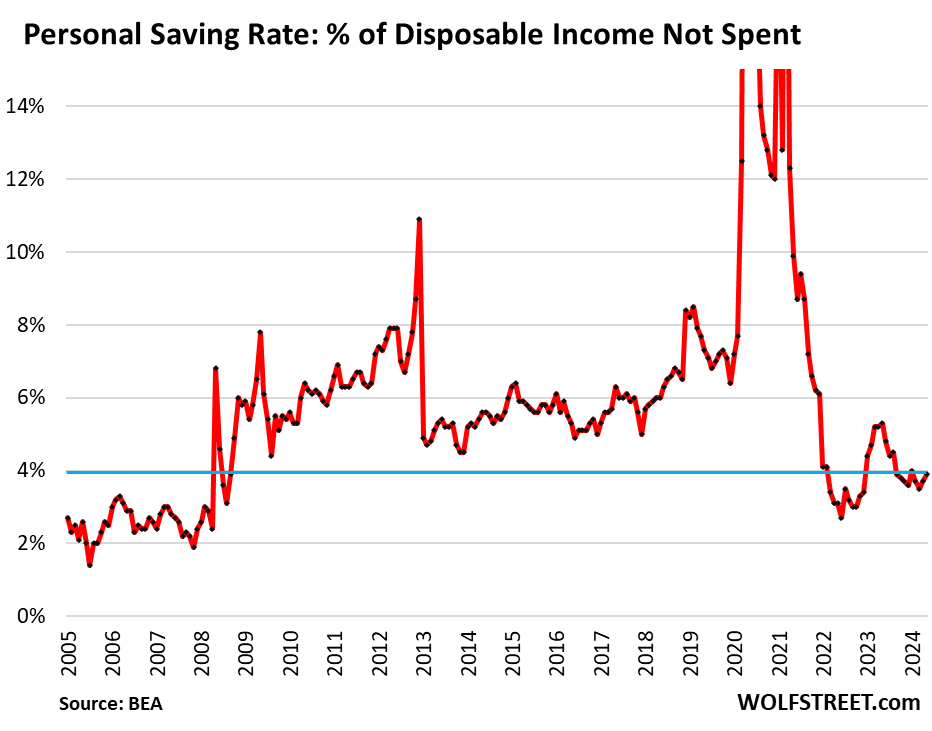

personal savings rate And it rose to 3.9%. That’s the portion of disposable income that consumers didn’t spend. That doesn’t mean they put it in savings accounts. They might have bought stocks with it, or left it in their checking account, or used it to pay off credit cards, or bought shares in a money market fund, or something else.

Americans are not big savers, and never have been. The money is there to be spent. But some are being saved anyway. The current rate is lower than it was in the decade before the pandemic, but higher than it was in the years before the financial crisis.

How our drunken sailors spent their disposable income:

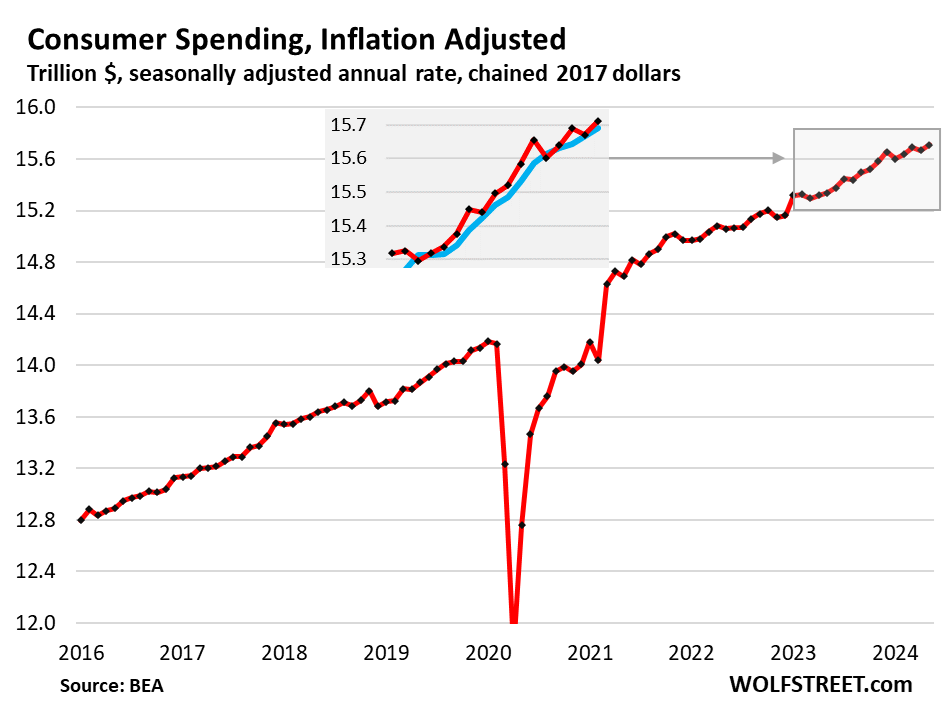

Consumer spending, adjusted for inflation, It rose by 0.3% in May compared to April, and by 2.4% compared to last year. They were spending more than pre-pandemic inflation: This “real” growth rate of 2.4% on an annual basis is within the range of good times in the years before the pandemic, which is not exciting, but very decent for the US economy.

To see beyond the monthly zigzags, we also look at the three-month average (in blue in the appendix), which has risen at a rate of 2.2% to 2.7% year over year over the past 12 months, in line with that of a typical US economy.

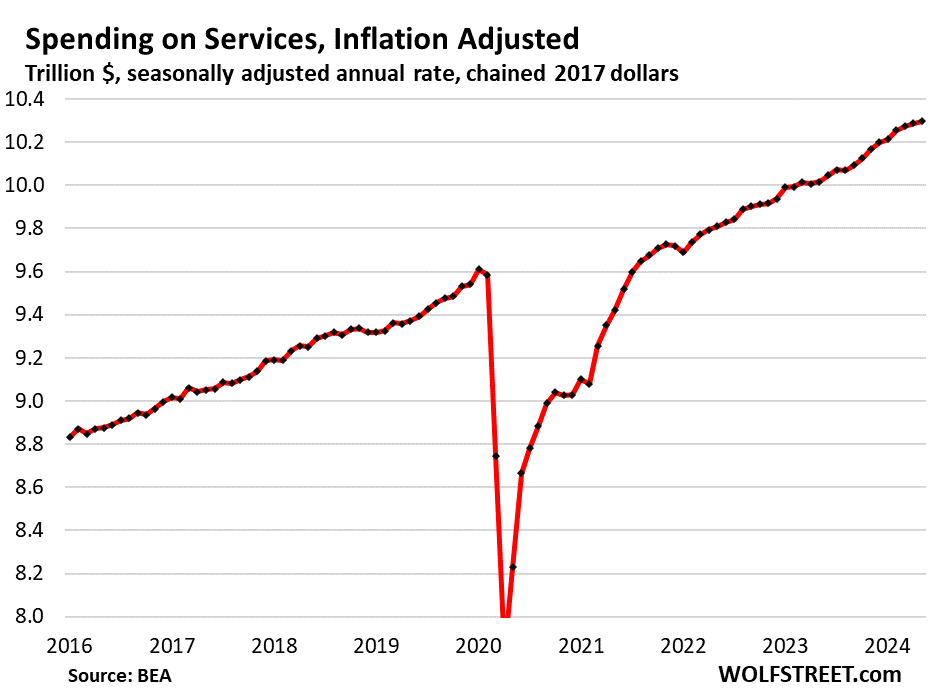

Spending on services, adjusted for inflationIt rose by 0.1% on a monthly basis and by 2.8% on an annual basis.

Inflation in services is high, and it is difficult to avoid it because many services are necessary, and consumers complain and grumble about inflation in services, but they still spend more than it, but barely.

Spending on services constitutes 65.5% of total consumer spending. This includes rent, utilities, insurance, streaming, broadband, mobile services, entertainment, healthcare, airfare, accommodation, car rentals, memberships, etc.

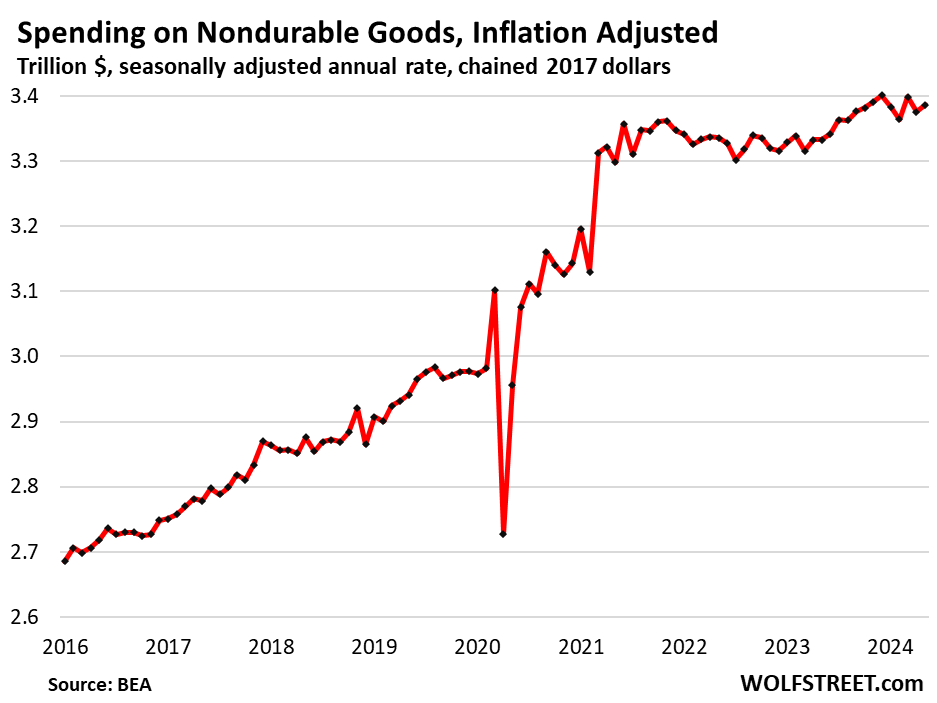

Spending on non-durable goods, adjusted for inflationNondurable goods prices rose 0.3% in May from April, and 1.6% on a year-on-year basis. Nondurable goods are dominated by food, gasoline, clothing, footwear, household supplies, etc.:

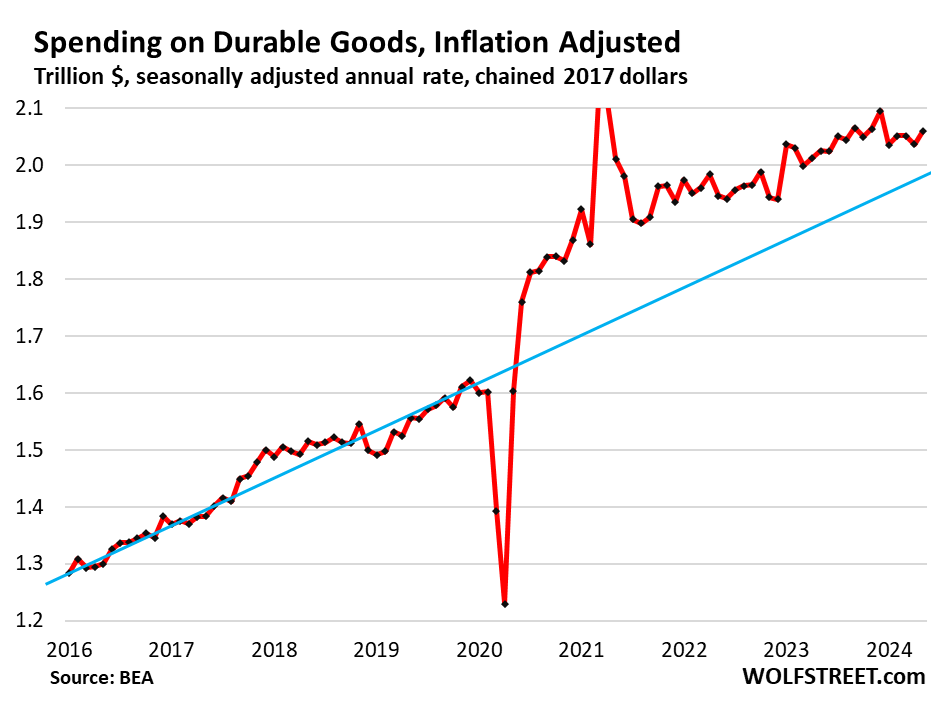

Durable goods spending, inflation adjustedIt jumped by 1.1% during the month after falling in the previous month. So, the three-month average got rid of some of that skewness, and was up 0.13% on a monthly basis and up 1.9% on a yearly basis. The pandemic appears to have permanently altered Americans’ high inflation-adjusted purchases of durable goods. The trend has never returned to normal, which is amazing:

Do you enjoy reading WOLF STREET and want to support it? You can donate. I would greatly appreciate it. Click on the beer and iced tea mug to learn how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()