LONDON, Sept 19 (Reuters) – Saudi Arabia’s oil minister denied the kingdom’s recent production cuts were aimed at raising prices, speaking at the World Petroleum Conference in Calgary on Sept. 18. .

“It’s not about… raising prices is about making the right decisions when you have the data,” he said (Saudi Energy Minister says oil cuts are not about raising prices) (Financial Times, September 18).

Energy Minister Abdulaziz bin Salman cited continued uncertainty about China’s oil consumption, Europe’s manufacturing downturn, and inflation and interest rate trends in North America and Europe.

He rejected predictions that the oil market would fall into a deep deficit in the fourth quarter, pointing out that supply and demand forecasts are not always reliable. Production cuts had to be made,” Reuters, September 18).

“My motto is that it’s always good to live up to the saying ‘believe it when you see it.’ If reality comes as predicted, hallelujah, we can produce more.”

He also criticized forecasts published by the International Energy Agency (IEA). “They have moved from market forecasters and evaluators to practitioners of political advocacy.”

But the IEA is not the only forecaster expecting a sharp decline in inventories, which are already well below long-term seasonal averages.

The very strong backwardation in futures contracts for the next six months suggests that the majority of oil traders share this view.

Chart book: Brent price and spread

inventory depletion

The additional production cuts announced by Saudi Arabia and Russia, if fully implemented, will remove a total of 125 million barrels of crude oil from the market by the end of September and 245 million barrels by the end of December.

At the same time, the economic outlook for the United States is improving, with growth accelerating, inflation slowing and the central bank expected to end, or at least pause, its interest rate hike campaign.

The combination of slowing oil production and accelerating consumption has changed the outlook for inventories, prices, and calendar spreads.

- U.S. commercial crude oil inventories, the most visible on the global market, have fallen by a total of 32 million barrels in seven of the last 10 weeks since the end of June.

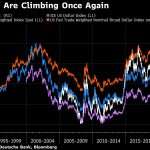

- North Sea Brent prices last month averaged over $91 per barrel so far in September (59th percentile of all months since 2000), up from $75 per barrel (41st percentile) in June, adjusted for inflation. It is rising.

- Brent’s six-month calendar spread declined from $1.33 (53rd percentile) in June to an average of $4.50 per barrel (94th percentile) in September.

It is impossible to prove with certainty the relative contributions of production cuts and faster economic growth.

However, given the large production cuts and modest upward revisions to economic forecasts, it is reasonable to believe that production cuts accounted for more than half of the rise in prices and spreads.

However, even after the rise in oil prices, taking inflation into account, the level remains modest compared to the high oil prices of 2007-2008 and 2011-2014.

In real terms, monthly prices would need an average of $110 per barrel to be in the 75th percentile for all months since 2000, and $146 to reach the 90th percentile.

From a producer’s perspective, real prices are still not very high and there may be room for further price increases without negatively impacting consumption or profits.

Related columns:

– Crude oil prices soar due to inventory outflow from Cushing (September 15, 2023)

– Hedge funds flow into declining US crude oil inventories (September 11, 2023)

– Crude oil prices rise due to depletion of US crude oil inventories (August 31, 2023)

John Kemp is a market analyst at Reuters.The views expressed are his own

Our standards: Thomson Reuters Trust Principles.

The opinions expressed are those of the author. They do not necessarily reflect the views of Reuters News, which is based on principles of trust and is committed to integrity, independence and freedom from bias.