(Bloomberg) — As 2023 draws to a close, the U.S. labor market will likely remain strong while wage growth continues to moderate, preparing for steady economic growth and lower inflation next year. It’s in order.

Most Read Articles on Bloomberg

Employment in the world’s biggest economy is expected to rise by 170,000 people in December, government figures showed on Friday. This will result in an increase in employment of approximately 2.7 million people per year.

The median forecast in a Bloomberg survey of economists showed that average hourly wages would rise 3.9% from a year earlier, the smallest annual increase since mid-2021. The unemployment rate is expected to rise to 3.8%.

Although the pace of employment has slowed, the resilience of the labor market supports the view that the economy will continue to expand, albeit at a slower pace, in 2024. This is consistent with the Federal Reserve’s latest economic forecasts. Federal Reserve officials also expect inflation to slow.

The central bank will on Wednesday release the minutes of its policymakers meeting in December, where officials signaled an end to their aggressive interest rate hike campaign. The Federal Reserve has decided to keep its benchmark interest rate unchanged at its highest level since 2001 and not raise rates further.

Quarterly forecasts showed Fed officials expect to cut rates by 75 basis points next year.

Bloomberg Economics says:

“Job growth is concentrated in two non-cyclical sectors, health care and government, with flat to negative growth in most industries. As a result, wage growth will slow in December. Although the Fed’s policy shift may have prevented recessionary movements in the labor market, the movement is not yet sufficiently clear and our base case remains one of sustained increases in the unemployment rate in 2024. is.”

—Anna Wong, Stuart Paul, Eliza Winger, Estelle Wu, economists.Click here for a full preview

Also on Wednesday, the government will release statistics on job openings across the economy for November. Economists expect the number of job openings to rise from last month’s lowest level in more than two years, consistent with moderate trends in labor demand.

The first week of the new year will also include a featured survey of manufacturing and services activity in December.

Meanwhile, in Canada, the December employment report released on Friday will reveal whether the labor market remains relaxed as 2023 ends.

Elsewhere, the possibility of higher inflation in the eurozone is likely to get the most attention, along with purchasing managers’ research in China, as investors settle in for the new year.

Click here to find out what happened last week. Below is a summary of what will happen next in the global economy.

Asia

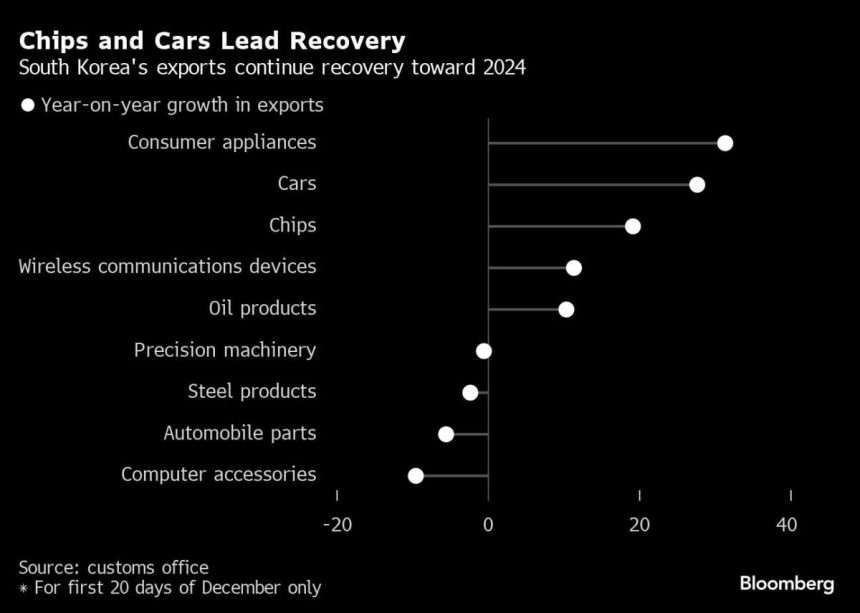

The year begins with December export numbers from South Korea. This is an early indicator of the health of global commerce and technology demand. Partial figures for the month already show continued momentum in overseas sales through the end of the year.

Also on Monday, Australian house price data will show how the Reserve Bank of Australia’s interest rate hikes, including the latest move in November, are impacting the property market.

China’s Caixin Manufacturing PMI follows official Purchasing Managers Index figures released on Sunday showing factory activity contracted to its lowest level in six months. This will serve as a further indicator of whether such a situation exists. -The peak of the festive season has passed for exporters.

Similarly, PMIs for several other Asian economies are expected to be released on Tuesday, giving a clearer picture of the regional economic situation at the start of the year.

Singapore’s economy is expected to slow on a quarter-on-quarter basis in the last three months of this year.

Countries will release inflation data throughout this week. Pakistan’s report will be released on Monday, Thailand’s report on Friday, and reports from Indonesia, Taiwan and the Philippines will also be released. India on Friday released new forecasts for its gross domestic product in 2024.

Europe, Middle East, Africa

A multi-year suspension of regional fiscal rules aimed at reducing debt ends in the eurozone on Monday, ushering in a new era of integration. The structure was tweaked by finance ministers in a last-minute agreement on December 20.

European Central Bank President Christine Lagarde said the euro gave Europe “greater sovereignty in a turbulent world” and the single currency also celebrates its 25th anniversary on Monday.

Her comments, published in a joint editorial with the leaders of the European Commission, Council, Parliament and Eurogroup, praise the survival of a financial arrangement whose collapse was often predicted.

For example, as the Greek crisis intensified in 2015, former Fed Chairman Alan Greenspan thought it was only a matter of time before everyone realized that parting ways were the best strategy. Greece did not leave, and the region instead welcomed Croatia as its 20th member in 2023.

That aside, ECB officials tend to remain quiet during the first week of the year. The bank is likely to focus on PMI figures for Italy and Spain, along with inflation data, ahead of its first year decision for 2024 on January 25.

On Thursday, France and Germany will release consumer price data for December, followed by Italy and the entire euro zone on Friday.

The energy base effect could push inflation to 3% from 2.4% in November.

It’s been a quiet week in the UK, with all eyes on final PMI figures, mortgage and consumer credit data, and the Bank of England’s Decision-Making Committee, a survey that helps outline wage risks.

Inflation in other regions may get the most attention. Turkish data on Wednesday could show consumer price growth accelerated by more than 62% month-on-month in December.

Polish data on Friday will reveal whether inflation has slowed to its weakest pace since September 2021.

Meanwhile, Israel’s first rate cut since the pandemic will be considered on Monday when the central bank reviews its policy. Economists are narrowly divided, but a slight majority, including most of the world’s financial institutions, expect a decline of one-quarter of a percentage point.

Israel’s central bank has repeatedly indicated that its focus is on maintaining market stability as the war with Hamas approaches three months, but the shekel has appreciated sharply and inflation is rising. As we slow towards $100, easing monetary policy is an option. The target range was achieved for the first time since early 2022.

As uncertainty remains high and the risk of a broader conflict, the Bank of Israel could postpone rate cuts for a longer period of time and wait until next year to begin cutting rates in parallel with the Fed.

latin america

Peru kicks off the Latin American new year with its December consumer price report on Monday.

Adrian Armas, the central bank’s chief economist, expects inflation to end 2023 near the target range of 1-3%, up from 3.64% in November, after several months of consecutive deflation. The central bank expects core print to reach its target range “by the end of 2023,” while headline reading will be achieved within “the next few months.”

The highlight in Mexico will be the minutes of Banxico’s December 14 policy meeting. Policymakers led by Governor Victoria Rodriguez accepted a proposal to keep interest rates on hold “for the foreseeable future,” leaving the key interest rate on hold at a record high of 11.25% for the sixth consecutive meeting.

The median forecast of economists in Citi’s latest survey is for one more rate cut in February, followed by a quarter-point cut in March.

December’s Purchasing Managers’ Index is likely to show that Mexico’s manufacturing sector continues to expand, while Colombia and Brazil remain in recession territory.

Brazil’s industrial production data for November, to be released on Friday, may reflect this weakness.

–With assistance from Paul Abelsky, Brian Fowler, Paul Jackson, Robert Jameson, and Laura Dillon Cain.

(Latest information on China PMI in Asia section)

Most Read Articles on Bloomberg Businessweek

©2023 Bloomberg LP