Bipartisan support for temporary additional government spending to preserve businesses and jobs through JobKeeper has been one of the few positive outcomes of the Covid-19 pandemic.

The recognition that the long-term damage caused by short-term economic crises far exceeds the cost of temporary government spending to avoid them has strengthened this consensus.

It is now worth considering whether the same logic could be applied to creating HomeKeeper, particularly in light of the Reserve Bank Governors. Michelle Bullock’s last letter That interest rates could remain higher for longer than expected.

JobKeeper kept businesses open and saved jobs during the brief pandemic economic crisis.

Likewise, HomeKeeper can help financially stressed mortgage holders avoid losing their homes during the current interest rate crisis, and prevent them from joining already long rental queues – or worse, becoming homeless.

The government can apply vital lessons from JobKeeper’s design flaws too, making HomeKeeper a winner not just for vulnerable mortgages, but also for the government’s balance sheet.

Stock struggle

How the HomeKeeper scheme works.

Instead of loans or handouts, the government can take a small stake in the property, equal to the value of the mortgage assistance as a percentage of the market value of the property at that time.

The idea is to give those experiencing mortgage stress a little breathing room to recapitalize and help them hold out until interest rates fall without having to lose their homes. Up to $25,000 in aid per household would be a reasonable cap.

It’s gonna work like this. Let’s say, for example, that someone has a $500,000 mortgage and their monthly payment is $5,000. They can apply for HomeKeeper assistance for five months (reaching the $25,000 cap). In return, the government will get a 5% stake in their home. This can also be obtained as partial assistance, depending on the homeowner’s needs.

Then, when the owner is able to repay the government’s share, or when the house is sold—whichever comes first—the government repays the market value of the equity share at that time.

These equity shares could be held in a government “housing fund” until they are repaid on market terms. This would reflect the growth in the capital value of the property and make it a sound investment for the taxpayer.

By keeping the maximum share size low, aid will be more meaningful to low-income families living in modest homes. Relative to the size of their mortgage, this would be a huge help, and could mean the difference between keeping the family home or having to sell.

Mortgage payments can be sent directly from the government to the relevant bank with the mortgagee’s permission, to ensure that the funds are used on time and for the agreed purpose.

Read more: What happens if I can’t pay my mortgage and what are my options?

Why is HomeKeeper necessary?

Australia has a crude system for determining mortgage stress.

In Research After the Global Financial Crisis (GFC), University of Western Sydney The Urban Research Center found a set of moleculesSometimes indirect measures use “asymmetric categories”.

She added, “There is often a failure to separate rich families from poor families.” In other words, the government tends to cite the big picture rather than the specific situation of different types of mortgages.

Stock struggle

There is also often an unofficial assumption that because Australia is fully employed, people will have no problem making their mortgage payments.

“Most families, because employment is so strong and unemployment is so low, seem to be coping,” says the Australian National University economist. Ben Phillips told the Australian Financial Review Last month.

However, Phillips acknowledged that Australia did not have recent and meaningful financial stress indicators. “Different measures such as arrears, insolvency, savings, etc. are partial measures or measures that are perhaps too late in the game,” he said.

So the image is opaque, and lags. The recession of the early 1990s showed how this happened It can actually do tremendous damage By the time governments realize its dimensions.

This ultimately had disastrous consequences for the Labor government that oversaw it.

The then Prime Minister, Paul Keating, won the 1993 election immediately after the recession, facing off against the leader of the New Liberal Opposition, John Hewson, who proposed a large new tax on goods and services.

But Labor lost the next election in a landslide, with voters sitting, in the words of Queensland Premier Wayne Goss, “on their balconies with baseball bats” waiting to vote Keating’s government out.

Banks classify loans as “defaulted” when mortgage payments are late. NAB CEO Ross McEwan told federal parliamentThe House of Representatives’ Standing Committee on Economics said in July that NAB was seeing “some stress in the system” and “an uptick in 30, 60 and 90-day delinquencies”, but said they remained below the 10-year average.

However, not all mortgages are created equal.

AMP Chief Economist Diana Mussina said in March “The downside risks to the household sector are greater than the Reserve Bank of Australia and most commentators estimate.”

Mussina drew attention to record Australian household debt as a proportion of household disposable income, which increases the scope of financial stress considerably, as well as to the particular vulnerability of one type of borrower.

In our view, the risk of mortgage stress falls on new borrowers who took out loans between 2020 and mid-2022, representing approximately 62% of outstanding home loans.

These families did not have enough time to build prepayment buffers […] They have had a very rapid repricing of mortgage rates, are likely to take out larger loans and may not have been stress-tested by the current increase in interest rates.

Read more: Homeowners often feel better about life than renters, but not always – whether you’re mortgaged or not

Helping those who do not have access to the “Bank of Mom and Dad”

Anecdotal evidence and logic suggest that there is another vulnerable group in addition to the one identified by Mossina: working-class mortgagees.

“Mom and Dad Bank” in middle and high-income families For some time, he helped the children buy their first home.

Another recent development is that Mom and Dad’s bank is offering assistance to help their offspring avoid mortgage delinquency in another intergenerational transfer of wealth among the wealthy.

But often there is no bank for mom and dad for working-class mortgage holders, who lack families with accumulated wealth to turn to for help.

HomeKeeper could be the government’s equivalent of a mom-and-dad bank for working-class families trying to hold on to their homes until interest rates fall.

Roy Morgan

What are the possible objections?

There are three main possible objections.

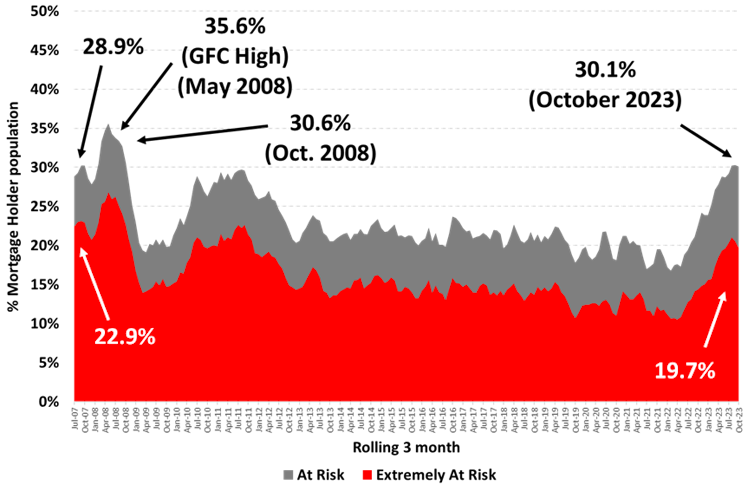

The first is that there’s no evidence of a problem that would require something like HomeKeeper to solve. However, current indicators are partial, inconsistent and lagging, so over-reliance on them is risky – and there are signs that there is already a problem.

Last Roy Morgan Stress Survey Among owner-occupied mortgages, it showed near-record numbers of people “in stress,” at 1,514,000, or more than 30% of mortgage holders. Nearly one million of them (967,000) are considered “extremely vulnerable.”

RedBridge pollster Kos Samaras has been regularly drawing attention to the extent of mortgage pressure in social media posts throughout the year.

By mid-2023, Samaras says, “more than 1.1 million borrowers in NSW and Victoria alone were experiencing negative cash flow” – that is, “insufficient income to cover repayments and other expenses”.

The second objection is that there have been assistance schemes in the past that did not work well.

It is true that there have been some small fragmented schemes, but none on a JobKeeper-type scale, or with a public profile at the level of JobKeeper, or with the sound financing characteristics of using equity shares rather than loans or handouts to fund them.

The HomeKeeper program will be different in type, size, profile and financial responsibility than any previous mortgage assistance program.

A third possible objection is that this would undermine the effect that higher interest rates are intended to have – specifically, to restrict household spending – and that interest rates would have to stay higher for longer to compensate for this.

This misses an important point.

Radiation therapy for cancer is used to apply obscenely large amounts of radiation to diffuse areas to achieve a desired goal, causing massive collateral damage in the process.

Over time, medical scientists improved their techniques and learned how to achieve the desired result using a much smaller amount of radiation confined to more targeted areas. These days, this science has become very precise.

There is no reason why monetary policy could not undergo a similar evolution, becoming less aggressive, more targeted and causing less collateral damage in the way it achieves the necessary goal of low inflation.

Working-class mortgage holders are not the kind of people who need to restrict their spending in the current inflationary environment. This should not be collateral damage in the RBA’s campaign to tame inflation.

A program like HomeKeeper can make the difference between them keeping their home or losing it, in a way that is good for them and their families, while at the same time being a sound investment for taxpayers.