Upcoming events:

- Tuesday: China Caixin Manufacturing PMI, Canadian Manufacturing PMI.

- Wednesday: Swiss Manufacturing PMI, US ISM Manufacturing PMI, US Job Opportunities, FOMC Meeting Minutes.

- Thursday: China Caixin Services PMI, US Challenger Job Cuts, US ADP, US Unemployment Claims, and Canada’s Services PMI.

- Friday: Eurozone Consumer Price Index, Canadian Labor Market Report, US Nonfarm Payrolls, US ISM Services PMI.

Wednesday

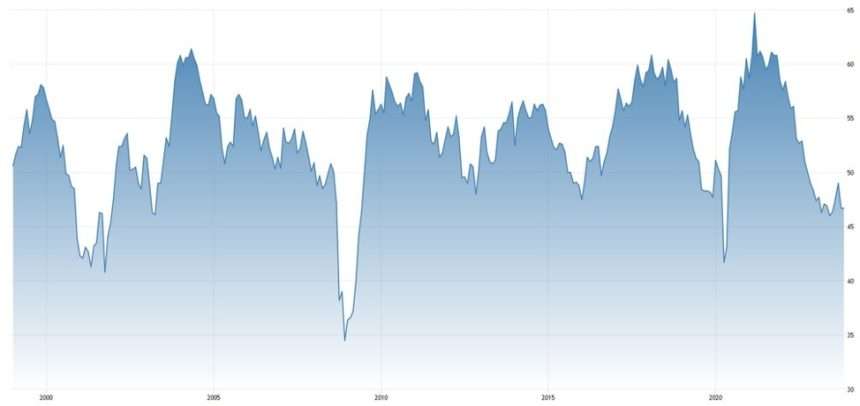

The US ISM Manufacturing PMI is expected to come in at 47.1 versus the previous 46.7. The latest report saw the index decline further in the contraction in November and Public comment was very bleak. Negative data It continued in December With the US S&P Global Manufacturing PMI violating expectations and confirming the pressure on the economy from the manufacturing sector.

US ISM Manufacturing PMI

The number of job opportunities in the United States is expected to reach 8.850 million, compared to 8.733 million previously. The latest report saw job openings fall much more than expected with the weakest reading since March 2021. Labor Market It continues to be mitigated by fewer jobs becoming available rather than more layoffsIt supports the narrative of a soft landing, which was coupled with a low inflation rate. But such events occur just before a recessionSo time will tell if “the busiest trade on Wall Street” is actually the right trade all along.

Job opportunities in the United States

Thursday

The US ADP report is expected to show 113,000 jobs added in December compared to 103,000 jobs added in November. The last report missed expectations, and of course, we got an overall win in the Non-Farm Payrolls report two days later. Although this version It is ineffective to predict the NFP numbercan be influential in the market and may give broad insight into the US labor market.

United States of America

US unemployment claims remain one of the most important releases each week because they are a convenient indicator of the state of the US labor market. Initial claims continue to hover around the lows of the cycle, which shows us that layoffs have not risen significantly yet, but continuing claims are rising at a rapid pace and this shows that people are finding it difficult to get another job after they are laid off.. Consensus this week expects initial claims to reach 215K vs. 218K previously, while continuing claims are expected to reach 1882K vs. 1875K previously.

US unemployment claims

Friday

Eurozone headline CPI y/y is expected at 3.0% vs. 2.4% previously, while core CPI y/y is expected at 3.5% vs. 3.6% previously. The market expects interest rate cuts of around 160 basis points in 2024, with the first 25 basis point cut in April. ECB members have been resisting aggressive market rates The consensus among officials is that they want to wait for the first-quarter data before deciding whether a rate cut in the second quarter will actually be justified.. Looking at the month/month inflation readings, the ECB can already call it “mission accomplished” and we could see year-on-year inflation rates falling to below 2% already in Q2 2024.

Core consumer price index in the euro area on an annual basis

The Canadian labor market report is expected to show 12K jobs added in December versus 24.9K in November and the unemployment rate rising to 5.9% versus 5.8% previously. This report is unlikely to influence the Bank of Canada’s January decision The central bank may want to see more data in the first quarter before deciding on the next step, especially after the recent hotter-than-expected inflation report. If you want to learn more about Canada’s forecast for 2024, you can read Adam’s articles about the Bank of Canada and the Canadian dollar.

Unemployment rate in Canada

The US Nonfarm Payrolls report is expected to show 163,000 jobs added in December compared to 199,000 jobs in November, and the unemployment rate to rise to 3.8% from 3.7% previously. Average hourly earnings are expected to decelerate further, with the annual measure expected to reach 3.9% versus 4.0% previously, and the mo/m reading at 0.3% versus 0.4% previously. Major central banks have ended their tightening cycles, so the markets’ reaction function has changed from “strong data equals more interest rate hikes” to “strong data equals fewer interest rate cuts.”

Unemployment rate in the United States

The US Services Purchasing Managers’ Index (ISM) is expected to come in at 52.6 versus the previous 52.7. The November report exceeded expectations The US services sector continues to remain resilient due to its low sensitivity to interest rate hikes. This trend was reaffirmed with the release of the S&P Global Services PMI for December, where data beat expectations to close the year with the fastest growth since last July.

Purchasing Managers’ Index (ISM) for US services